Where the Stock Market Will End 2019

Yesterday we ventured a cowardly 2019 forecast, in humble recognition of our erring psychic vision.

Markets would rise, we soothsaid — or fall — or end the year precisely where they began.

We likewise predicted the economy would advance, retreat or jog in place.

Some readers denounced our abject cowardice.

Take your stand upon one hill or the other, they thundered. But take your stand:

“Make a call,” demanded one reader, Michael by name. “We are counting on you to make actual predictions…”

“Please do not waste my time with something that says nothing,” argued another reader, Richard.

A third — Gary — believes our dish of applesauce actually diminished his cognitive powers:

“I think I lost IQ points in reading the article… So you know nothing…. Why publish it?”

Our character thus slandered, today we summon our best blood — “not the blood of our finger but the blood of our heart”…

And come out flat-footed with a 2019 forecast guaranteed to keel you over.

First we train our sights on a far more immediate vista — today’s market activity.

But perhaps it is best we not…

The Dow Jones hemorrhaged another 660 crimson points today.

The S&P lost another 62. The Nasdaq shed 202 dreadful points — a 3% trouncing.

What accounted for today’s thunder and lightning?

A falling Apple, primarily.

Apple slashed its quarterly revenue forecast late yesterday — for the first time in over 15 years.

CEO Tim Cook cited an “unforeseen” slowdown in the Chinese economy.

And so a bellwether of global economic conditions presents a distressing omen. Explains Greg McKenna, markets strategist at McKenna Macro:

That Tim Cook and his company mentioned China as the reason behind the downturn in the company’s outlook seemed to hit exactly the pressure point traders and investors were already alarmed over.

Apple stock plunged 10% today… incidentally.

But it was not Apple alone that frightened the horses today…

The Institute for Supply Management reports that U.S. manufacturing has plunged to a 15-month low.

Manufacturing sentiment also suffered its largest one-month drop since October 2008 — when the financial crisis was in full blast.

On that note…

We are reliably informed that global liquidity is evaporating at its fastest clip since 2007–08.

According to analyst Michael Howell of the CrossBorder Capital blog, global liquidity has slipped some 25% below its long-term trend.

The Federal Reserve is driving the business.

It is tightening financial conditions far more than generally realized… once we account for quantitative tightening.

Howell estimates the “true” fed funds rate is not the official 2.5% — but closer to 5%.

“In other words,” says he, “tight liquidity conditions are equivalent to the Fed undertaking around 20 rate hikes rather than the nine it has so far implemented this cycle.”

Thus the ground is laid for another 1997 Asian crisis — though not limited to Asia:

Unlike the 2007–08 crisis, which was more about a broken banking system involving the sudden collapse of leverage among overextended banks and shadow banks, the current credit squeeze looks more like the 1997–98 Asian crisis when central banks, led by the U.S. Fed, tightened the supply of primary liquidity… This time around, financial markets are probably even more interconnected and more global. Consequently, this could be an Asian crisis-like sell-off, but one not only confined to Asia.

Perhaps someone should alert Jerome Powell?

But to return to our thumping market prediction…

We have suggested previously that the Federal Reserve’s most recent rate hike may have taken the fed funds rate over the “neutral rate.”

That is, interest rates are no longer “accommodative.”

Nor are they merely neutral.

They begin to drag and tug.

History suggests recession or market crisis is on tap six–12 months after rates cross the neutral line.

Furthermore…

The stock market generally turns in its worst performance six months preceding a recession.

Well, it has pointed south since early October — for precisely three months, that is.

At present speed and heading, the economy is on course for recession by April perhaps.

Unless, that is, the stock market finds a fair wind beforehand.

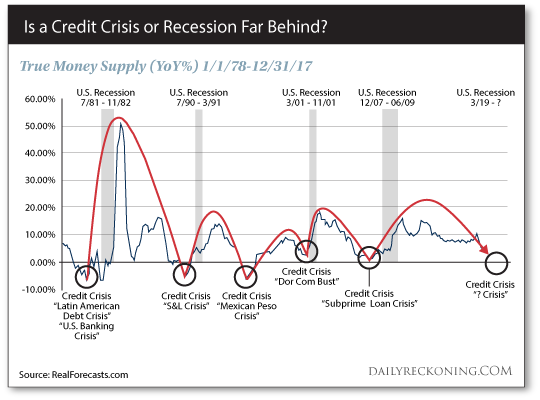

We have further furnished evidence that the “true” money supply is falling violently (see linked article for details).

Let the record show:

Recession or credit crisis followed previous occasions when the true money supply decelerated at the present clip:

The chart suggests trouble starting in March.

In conclusion… we have strong circumstantial evidence pointing to recession sometime this year.

March 1 — incidentally — is when Trump’s hard trade deadline with China lapses.

If no accord is reached by March 1, the trade war resumes at full pitch.

Mixing it all together, let us proceed to our rafter-shaking 2019 forecast:

Trump realizes the extent to which his presidency hinges upon a thriving economy and stock market.

He will therefore settle upon a deal and declare resounding victory.

The stock market will rally hard on the news.

But it will be short-lived.

Political uncertainty will play the devil with markets…

The Mueller investigation will soon come out.

We hazard it will reveal no evidence whatsoever of Russian collusion.

But give a man nearly two years and millions of dollars to find skeletons in closets… and he will find skeletons in closets.

Especially, we may add, if he ransacks the closets of a horse trader like Donald John Trump.

Once the Democrat-controlled House impeaches Trump — yes, that is correct — exhausted markets will lose remaining steam.

This will drag on much of the summer.

Trump will survive — the Senate will not convict him of charges — but the process will leave him severely diminished.

Meantime, markets will confront the reality of drying liquidity… and economic growth will slow to a glacier’s pace.

The economy will finally be in recession by December.

The stock market will likewise end 2019 sunk in a bear market…

The Dow Jones will end the year at roughly 18,000.

The S&P will hold above 2,000 — but barely.

The Nasdaq will take a good 40% lacing from today’s levels.

Gold will challenge $1,500.

There is your preview of 2019, down to the last jot and tittle, down to the last decimal point — and you can just take it to the bank.

Never you mind our last prediction. Or the prediction prior. Or…

Regards,

Brian Maher

Managing editor, The Daily Reckoning

Comments: