The EM Outperformance Cycle

Occasionally I come across a chart so fascinating, I know right away it’s going to be the focus of my next newsletter.

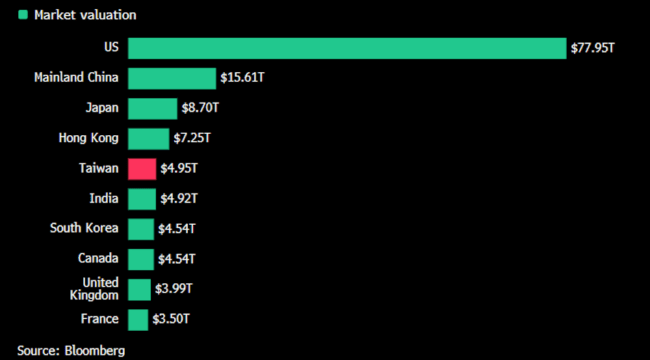

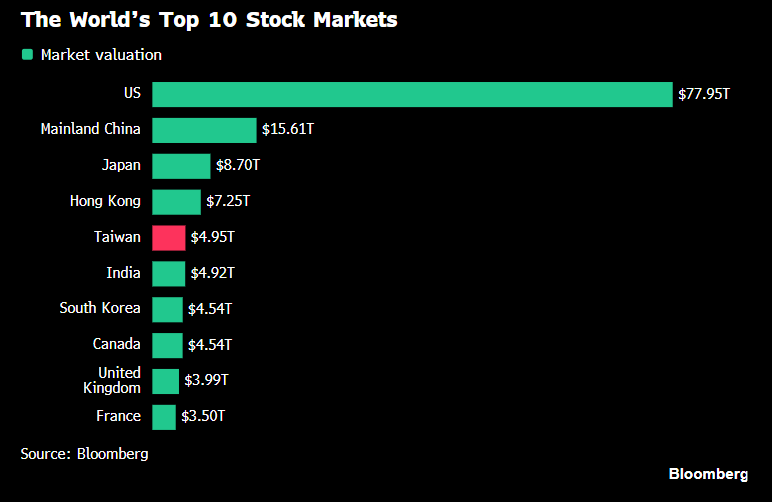

Here’s the latest one. It shows the valuation (market cap) of the world’s top 10 stock markets by country.

America’s stock market is currently bigger than the next 9 largest combined. By a wide margin.

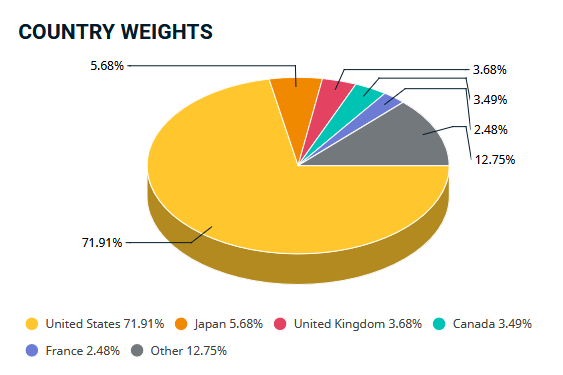

In the MSCI World index, the U.S. makes up a whopping 72% of the total. That is despite only making up 26% of global GDP. (Note: The MSCI World index only includes “developed” markets such as European countries and Japan.)

Source: MSCI

The MSCI World index is supposed to represent the “world”, but today it’s 72% American stocks. The MSCI World index is used by ETFs and institutional investors to allocate their investment strategies.

This is primarily a result of American stocks crushing the rest of the world over recent decades. That, and the U.S. dollar’s strength due to being the world reserve currency.

The second largest country behind the U.S. is Japan, with 5.68%.

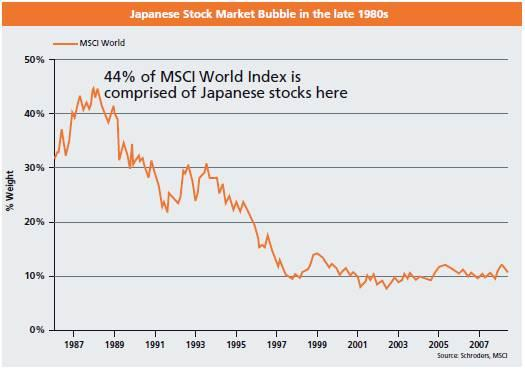

But here’s a shocker. Back in the 1980s, Japan peaked at 44% of the MSCI World index!

Japan’s stock market was actually bigger than the U.S. in the late 1980s. And Japan had roughly a third as many citizens. At that time, Japan was seen as an unstoppable force. It was dominant in cars, electronics, and other manufactured goods.

Japan’s stock market peaked in 1989. And it took until 2024 to surpass that late 1980s peak. The result was 3+ decades of horrible performance in Japanese stocks. Their market is starting to turn around today, but 35 years is a long time to wait…

Can America’s Run Continue?

That’s the big question. Can the U.S. keep stomping every other stock market into the dirt? Or will the cycle turn, as it always does?

Well, U.S. stocks are currently priced at nosebleed levels. The S&P 500 trades at an average P/E of around 28. That means if the average company paid out 100% of its earnings as dividends, it would take about 28 years to get your money back. And that’s assuming there were no taxes paid. It also assumes no earnings growth (or drops), so those two factors should roughly cancel out.

One other factor to consider: American markets today are HEAVILY tilted towards technology. Nvidia (NVDA), for example, makes up 6.5% of the total U.S. market by itself. So there are also serious concentration risks to consider. It works great on the way up, but not so much on the flip side.

Here’s how America’s valuations stack up against other global markets.

Global Stock Market Valuations (Price/Earnings) by Country ETF

- U.S.: 28 P/E (SPY)

- Brazil: 12 P/E (EWZ)

- China: 9 to 14 P/E (FXI and MCHI)

- Germany: 16 P/E (EWG)

- India: 23 P/E (INDA)

American companies are priced at very expensive levels, especially compared to markets like Brazil, China, and Europe. India is also expensive, which is why I avoid it.

Now, there is a reason for that American premium. We’re the home of innovation. New technologies are born here. And the dollar, despite its flaws, remains the world’s reserve currency.

However, the premium has gotten to extreme levels. And most Americans own few foreign stocks. And they own even fewer emerging markets (EM) like Brazil. Personally, I’m much more interested in EM than Europe. So that’s what we’re going to focus on.

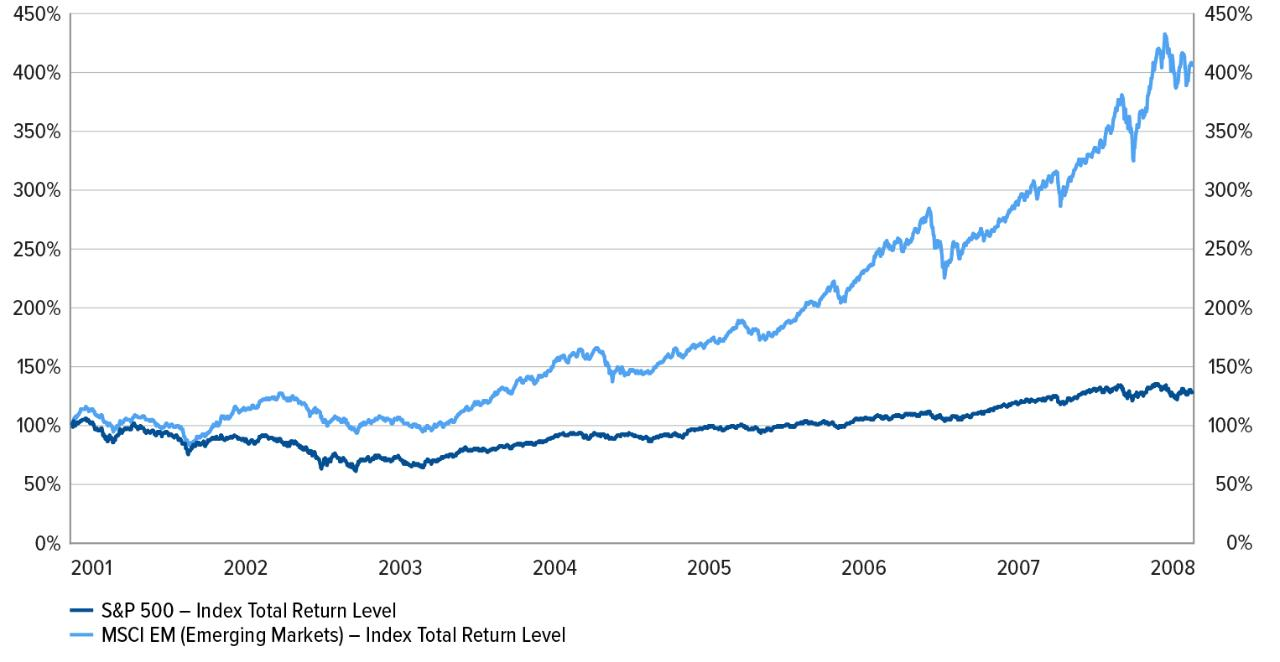

I believe we are now entering a period when emerging market stocks will outperform the U.S. The chart below shows what that can look like. The S&P 500 is in dark blue, and the MSCI Emerging Markets index is in light blue.

So from 2001 to 2008, emerging markets outperformed the U.S. by more than 3x.

It’s a cycle. American stocks hit the ball out of the park for a while, and eventually they become overvalued. By that point, everyone has forgotten about emerging market stocks, and has almost no exposure. So EM is cheap, yields are high, and a rotation out of the U.S. and into EM begins.

I think that’s where we are today. EM stocks are finally waking up after 15+ years of underperformance. Brazil, which we’ve been highlighting for more than a year, is up 30% over that time, despite its recent pullback. That’s slightly above the S&P 500’s 28% return, in the midst of AI mania.

Once you factor in the relative valuations, EM is simply too cheap to ignore. American stocks are priced for perfection. EM is priced for an asteroid strike.

And no, I’m not saying to sell your U.S. stocks. They’re on a record run. But it won’t last forever.

So consider adding some emerging market exposure to your portfolio. The simplest way to do so is to own a large diverse ETF like Vanguard’s VWO. This gives broad exposure to the EM universe, and the expense ratio is a rock-bottom 0.06%. That’s practically free.

My favorite EM play remains the iShares Brazil ETF (EWZ). EWZ has pulled back from its recent highs, but is still cheap, high-yield, and in an uptrend.

Today, most of the world is overweight American stocks. And it’s worked out extremely well over the past 15 years. But now is the time to start diversifying.

When this AI mania eventually ends, it will pay to have significant exposure to emerging markets. Just as it did after the dotcom era, from 2001 to 2008.

Comments: