Delayed Impact

In October 1973, Arab oil producers slashed exports to the U.S.

This was in the middle of the Yom Kippur war, a brief but intense conflict between Israel and a coalition of Arab states.

Saudi Arabia and other Arab OPEC members were angry about America’s support for Israel. So they refused to send oil to us for a while.

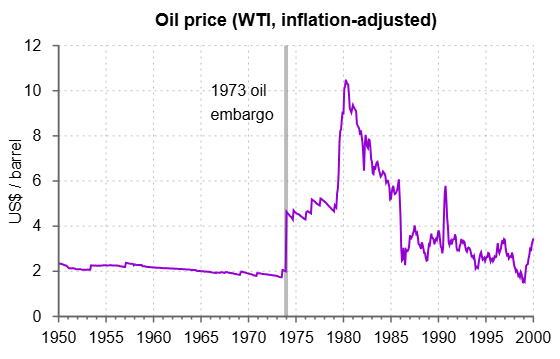

The price of fuel jumped. Here’s a chart of oil prices from 1950 to 2000 (note: this chart is inflation-adjusted, but shows the spike in 1973 clearly).

Oil prices quickly doubled. At peak, the price of a barrel increased more than 4x from early 1973 levels.

Oil never returned to pre-embargo levels, except for a brief dip around 1998 (in real inflation-adjusted terms). Despite the embargo only lasting 5 months.

Chaos in the Middle East tends to create… more chaos. After the Yom Kippur war, there was the 1979 Iran revolution, which kicked Western oil companies out of the country (and set the stage for today’s confrontation).

Then we had the Iran-Iraq war, which severely disrupted production and shipping once again. Then the first Gulf war against Iraq, and then the Global War on Terrorism.

The 1973 crisis was caused by about a 5% drop in oil supply. What we’re looking at today is a roughly 13% decrease. Which could rise to 20% if the Houthis shut down the Red Sea as well.

Of course, we’re just now approaching two months into this disruption. But if it goes on much longer, the impact will be far more significant than the ‘73 embargo.

Stocks: A Delayed Reaction

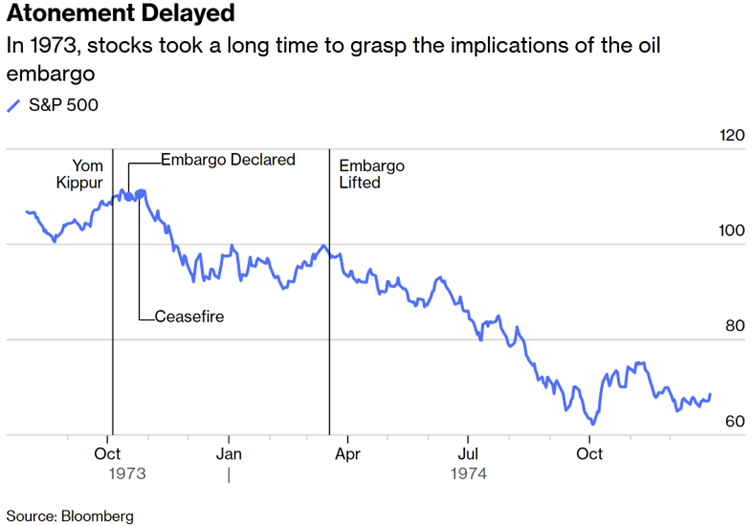

During the five months of the 1973-1974 oil embargo, the S&P 500 fell about 10%. Investors weren’t too concerned, at first.

What’s interesting is that stock markets fell sharply after the embargo was lifted. It almost looked like a classic “sell the news” reaction:

In the 6 months following the embargo being lifted, U.S. stocks fell another 35%. Oil prices remained high, and pre-existing problems didn’t magically disappear.

The economic damage was ongoing. Investors just hadn’t digested it yet. Government measures such as price controls ended up making things worse.

Inflation led to less consumer spending, which caused economic slowdowns, which led to the Federal Reserve printing gobs of money, and cutting interest rates prematurely.

This was the 1970s stagflation story in a nutshell. It lasted 7 years after the embargo ended.

Not Out of the Woods Yet

Whenever this mess is over, let’s hope oil doesn’t continue rising like it did after the 1973 embargo. But prices will stay elevated for longer than most investors expect.

In the best case scenario, if this ends soon, we’re still looking at significant damage to oil infrastructure, and pent-up demand.

Nations will have to rebuild strategic petroleum reserves. And many will greatly expand their emergency fuel storage capacity, then fill it up. This alone will keep a bid under oil for a while.

And in a less rosy scenario, the war resumes and escalates. Unfortunately, this looks increasingly probable.

Jim Rickards has been warning about this for a while. In Monday’s Five Links, he told Strategic Intelligence readers that America and Iran are incredibly far apart on their deal expectations. And warned:

The U.S. is surging special forces, aircraft carriers and Marine amphibious landing units to the area.

Does this sound like the war is ending?

All signs point to more fighting, escalation, higher energy prices, energy scarcity and a major global recession or worse. Trump’s cheerleading won’t change that. Markets need a reality check. They may get one soon.

The man has a point. Another U.S. aircraft carrier strike group is heading to the Middle East as we speak. Missiles, bombs, and planes are being flown and shipped in from bases around the world.

And negotiations are going nowhere. We’re back to “passing notes” through Pakistan. When the two sides of a conflict can’t even negotiate directly, it’s unlikely a deal is near. Distrust runs high on both sides.

So it’s possible this ceasefire is nothing more than an intermission, as we discussed a few weeks back.

I truly hope that’s not the case. But for now the Strait of Hormuz remains closed to 99% of traffic. And as Jim Rickards noted today in the Paradigm Press app’s Daily Feed, that’s the only signal that truly matters. Everything else is noise.

Yet stocks continue on as if everything’s normal. In 1973 we saw a similar reaction, at first. Then stocks dropped 35% in 6 months.

We could see something like that play out again. At this point, downside risks far outweigh upside potential in most U.S. stocks. They’re too expensive to buy here for anything other than a trade.

In my long-term portfolio, I continue to have oversized allocations to hard assets, precious metals, and cheap high-yield emerging market stocks. More on those soon.

Comments: