Worst Case Scenario – Rejected

With the Iran war winding down, now is a good time to review what we’ve learned.

Unless something catastrophic derails the deal, the Strait of Hormuz will soon be fully open again.

Oil, natural gas, fertilizers, and more will once again flow freely through the world’s most critical naval chokepoint.

Today, let’s review what we learned about energy and the global economy from this conflict.

Exaggerated Damage?

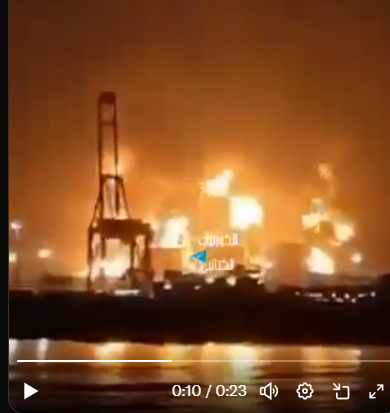

In mid-March, when Iran struck Qatar’s massive Las Raffan liquified natural gas (LNG) hub, the situation looked dire.

LNG is a critically imported fuel and feedstock. It is used to generate electricity, is a key ingredient to make fertilizers, and provides heat and cooking fuel.

Qatar produces about 20% of the total world supply of LNG. So when Iranian missiles struck their primary hub, it looked bad.

Qatar’s Ras Laffan LNG hub

Qatari leaders came out and said at least 17% of output was down, and it would take 3-5 years to repair the damage.

Additionally, the shutdowns caused by the Strait being closed reportedly caused all sorts of problems that would take a long time to fix.

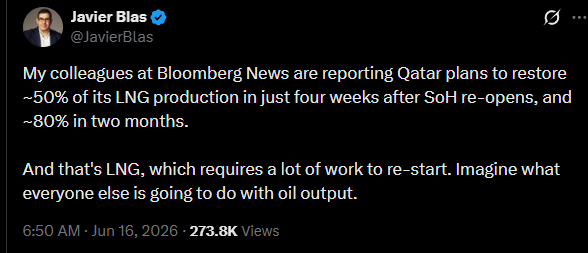

But now, we’re hearing a more optimistic story. Bloomberg energy specialist Javier Blas reports that Qatar’s LNG output will be back to 80% within 2 months.

Source: X

Now, we won’t know how bad the damage to Gulf oil wells and refineries is for a while. But in the heat of the moment, some of these damage estimates were probably too severe.

In hindsight, this makes sense. Qatar and other major energy producers had an incentive to overstate damage. “You’ve already damaged us enough, we won’t recover for years!”

The deception, if it was one, worked for both sides. Iran got to claim precise and asymmetric missile strikes, while the countries escaped without extreme lasting damage.

China: Tougher Than We Thought

There was a theory floating around at the beginning of this war that it was essentially a move against China.

The idea was straightforward. Since China normally imports 11 million barrels of oil per day, largely from the Persian Gulf, a major war and possible shutdown of Hormuz would cripple the country.

I don’t think the Iran war was primarily aimed at China. But if it was, it failed.

Beijing was clearly prepared for such a situation. Here’s are 3 factors which prevented shortages in the country:

- Electric cars – More than half of new cars in China are now electric

- Oil reserves – China has the largest oil reserves in the world at 1.5 billion barrels

- Coal-to-liquids – The country has made huge strides in converting coal to diesel and other petroleum substitutes

Before the war, the perception was that China’s Achilles’ Heel is Middle Eastern oil. But the country didn’t even dip into its oil reserves until mid-May, and even then they were drawing less than the U.S., at just half a million barrels per day.

Last month, China even began to export jet fuel and diesel to neighbors who faced severe shortages. This was… unexpected.

Over the past decade, China has electrified its transportation networks, built pipelines from Russia, developed its own oil industry, and stockpiled a huge amount of crude.

China is preparing for a world in which it no longer requires huge volumes of oil from the Middle East. This is a very important takeaway. It makes the country more resilient to energy shocks, and less vulnerable to economic warfare.

Worst Case Scenario – Rejected?

At the start of 2026, WTI Oil (American crude standard) was trading at about $57 per barrel. Today we’re at around $77.

It will take a while to restore traffic in the Strait of Hormuz to pre-war levels. There are mines to be cleared, and logistics to be worked out.

Then the world will need to refill strategic oil reserves and storage tanks. So oil prices are going to be higher than normal for a while to come.

But we didn’t reach the catastrophic shortages some (including me) thought would happen. Oil didn’t hit new highs, or stay above $110/barrel for long.

However, the spike in oil, fertilizer, and gas prices did hurt both consumers and commercial interests.

It put a serious strain on emerging economies, and we won’t know how badly the fertilizer shortages will affect food production for a bit.

Inflation will likely remain elevated for some time to come. But it looks like we escaped the worst-case scenario.

That doesn’t mean that stocks will keep rising forever. We’re getting a gnarly selloff today, and it could continue for a while. I continue to like hard assets, precious metals, and emerging markets over hot sectors like tech.

Israel, Lebanon, and Iran

Now, it’s still possible that something derails the peace deal and we re-enter crisis mode. Israel, our primary partner in the war, is clearly not happy with the proposed deal.

Personally, I think these issues will be figured out without a return to active conflict. There’s too much at stake. BUT… if anything goes wrong, it will likely involve these issues.

As part of the memorandum of understanding (MOU), the war is supposed to end on “all fronts, including Lebanon”. But Israel says these operations are necessary to prevent Hezbollah from striking settlements in the North of the country, and IDF forces near the border.

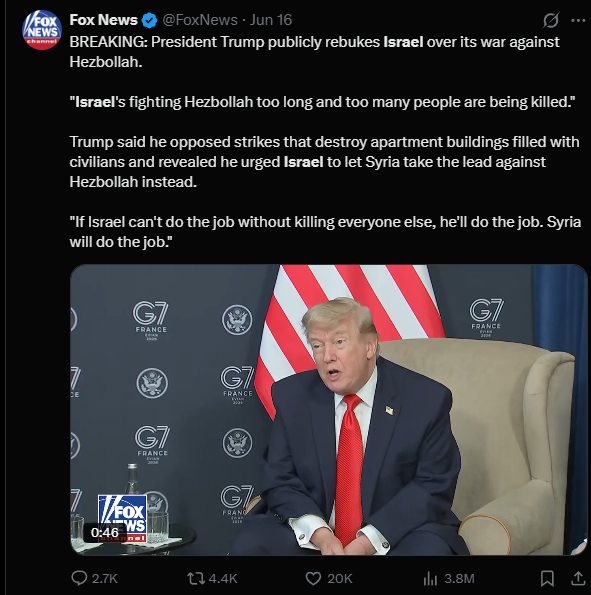

There is clearly tension developing between President Trump and Israeli leadership.

Source: X

Trump’s statements are interesting, and a bit worrying. What is this about letting “Syria take the lead against Hezbollah instead”?

That would just be a different kind of war. I suspect he’s frustrated that the Lebanon vs. Israel issue is a main issue holding up a deal, and is looking for a different path. But Iran is clearly determined to protect its Hezbollah allies/proxies. Syria will likely want nothing to do with fighting Hezbollah.

President Trump is clearly motivated to get the Iran issue resolved ASAP. That’s the important thing. Midterm elections approach. And if Hormuz stays shut much longer, we will actually reach those crisis levels. So I believe the deal will get done.

Still, it’s important to review this issue. If anything goes wrong, it will likely revolve around it. However, I doubt we’ll return to a situation where Hormuz is closed and the war restarts fully. We’re on a path to a (more) peaceful period in the Middle East. For a while, at least.

What to do with Oil Investments?

I’ve written quite a bit about Brazilian oil giant Petrobras (PBR, PBR.A). Most oil majors have fallen quite a bit from their wartime highs, including PBR.

But a falling oil price isn’t actually that bad for Petrobras. Due to the way the Brazilian government sets gasoline and diesel prices in the country, Petrobras has been forced to essentially subsidize the entire country.

Now, with falling oil prices, that pressure will be relieved. Yes, Petrobras will earn less from exports. But they’ll still be making plenty with a ~$40 all in cost per barrel.

Personally, I’m holding onto Petrobras and plan to reinvest the dividend for years to come. I might lighten up a bit sometime this year, because it became a rather large position, but this is one I plan to hold for years to come. It’s a nice pair trade with my gold and silver miners.

Needless to say, we’re keeping a close eye on the Iran situation and will keep you all well updated.

Comments: