The Elon Premium is Real

The SpaceX IPO next week is going to be nuts.

It’ll be a bit like the Superbowl for investors, on steroids. But bigger.

The valuation (market cap) of SpaceX at IPO is expected to be around $1.75 trillion.

I remember when Facebook went public at $104 billion and thinking that was crazy. SpaceX is going to be almost 17 times larger.

Today, let’s go through the SpaceX math and try to figure out if this stock is a buy.

A Hefty Price

$1.75 trillion is such a large number, it’s hard to wrap one’s head around it.

To understand the scale, here’s a simple framework. One million seconds is 11.5 days. One billion seconds is 31.7 years. One trillion seconds is 31,688 years.

An IPO of this size has never happened. Nothing else comes close.

So what are investors getting for this price?

In 2024, SpaceX made a profit of $791 million. In 2025, it lost $4.94 billion. In the first quarter of 2026 alone, it lost another $4.28 billion.

SpaceX has a highly profitable space launch business, and Starlink. So what happened? The company merged with X (formerly Twitter) and xAI, Elon’s social media and AI firms.

And as we all know, AI is a highly expensive business. GPUs and data centers aren’t cheap, and Elon’s company has rapidly built some of the largest AI compute clusters in the world.

The company’s Colossus data center clusters operate around 230,000 high-end Nvidia GPUs. The best AI hardware on the planet, at a scale that essentially nobody else has.

And xAI will soon start monetizing this asset at scale. They signed a deal with Anthropic, maker of the famous Claude AI models, which will reportedly generate about $1.25 billion in revenue per month.

That should get them close to breakeven by itself. And there’s a good chance that Elon’s proprietary AI model, Grok, will eventually catch up with ChatGPT and Claude in terms of capability.

Still, AI is an extremely competitive business. And believe it or not, SpaceX is mostly an AI company.

Sure, there’s a great space launch business, and the Starlink satellite communication network, which is still growing at 100% year-over-year. In 2025, Starlink produced $11.6 billion of revenue. That’s going to be a very nice business.

But much of the risk (and upside) in this stock comes from the AI side of the business. The company is investing massively in data centers and to build Grok, their proprietary AI model.

The Elon Premium

Elon Musk is the greatest American entrepreneur of the century. Paypal, Tesla, SpaceX, the Boring Company. It’s quite a track record.

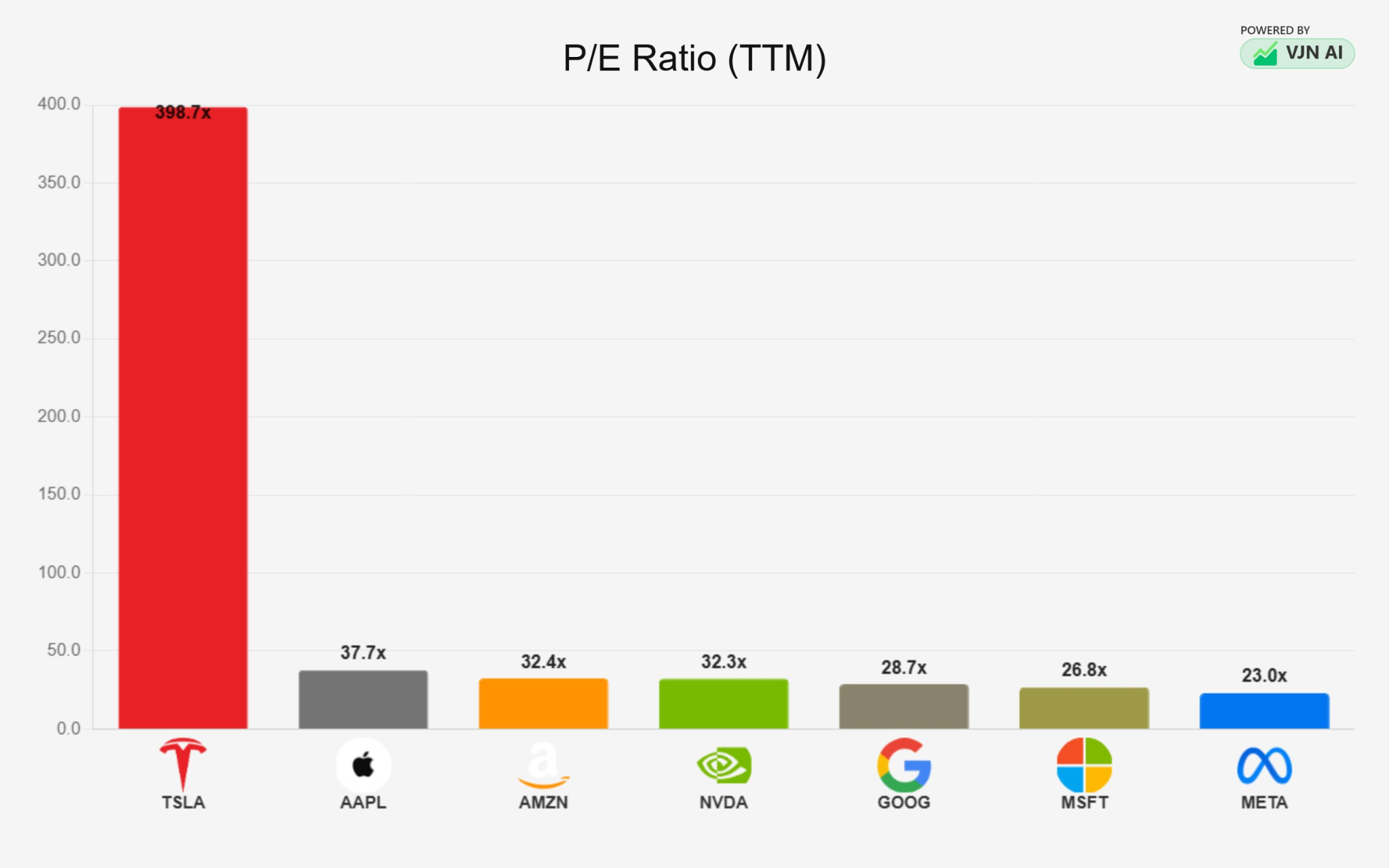

Tesla has created thousands of millionaires. And that stock isn’t exactly cheap either. The chart below shows the P/E ratios of the “Magnificent 7” tech stocks. Note how much more expensive Tesla is than everyone else.

People have been calling Tesla overvalued for many years, and it has simply maintained a premium price. Elon’s die-hard fans are convinced he’s going to win self-driving cars, and humanoid robotics. And those are both going to be massive markets. This is the Elon premium.

So it’s entirely possible that SpaceX starts out expensive, and simply maintains its valuation. Or even jumps higher.

But personally, I’m not buying the IPO. It’s too expensive for my taste. Based on 2025 revenue of $18.7 billion, it will debut at a rather expensive 94x sales (revenue). That’s… generous.

But hey, I’ve had the opportunity to buy SpaceX in private markets since it was around $100 billion, and I never pulled the trigger. It always seemed too expensive. Clearly, that was a mistake.

The core space launch business is fantastic. Starlink is amazing. And AI has massive potential.

If Grok becomes competitive with ChatGPT and Claude (the top 2 AI models), it could certainly justify the price. The parent companies of those two models (OpenAI and Anthropic) are both valued around $900 billion. And they don’t have a space business to go along with it.

The Elon premium is very real, and perhaps it can even support this massive valuation. However, I do worry about what would happen to SpaceX if we get a market crash. Even Elon’s giant cult of personality may not be able to maintain such a lofty price if the market tumbles.

For me, however, SpaceX is simply too expensive. So I’m steering clear. We’ll know next week whether that was a mistake or not.

Comments: