How to Invest in Junior Miners

Yesterday, we did a deep dive on one of the largest gold miners in the world, Barrick (B).

Today, we’re going to explore a smaller (junior) miner.

There’s no clean definition of what makes a miner “junior”. But it generally means smaller producers, as well as companies that are in the exploration or development stage.

Junior miners can produce big gains for long-term holders. But there’s also higher risk. Political risk, execution risk, and market risk.

As an example today, we’re going to look at Aris Mining (ARIS). Aris is on the larger side for a “junior”, but I didn’t want to pick anything too small and illiquid for this newsletter, which is read by more than 100,000 people.

I don’t own the company, and Paradigm never takes money from the stocks we cover. I mention this because it’s important, especially when it comes to junior miners. The mining world is full of stock promotion and if you’re not careful, you’ll end up buying a tiny stock someone else is being paid to promote.

First up, some basic ARIS stats:

- Market cap: $3 billion

- P/E ratio: 17.8

- 2025 gold production: 257,000 oz

- 2026 gold production guidance: 300,000 to 350,000 oz

- Revenue (last 12 mo): $1.1 billion

- Net debt: $2 million (low)

- FCF: $173 million (last 12 mo)

Aris operates in South America, primarily Colombia, but also has a mine under development in Guyana.

Now let’s dig into a repeatable framework we can use to analyze junior miners.

Start With the Presentation

Whenever I’m examining a new potential mining investment, I start with the corporate presentation. Every public mining company has one.

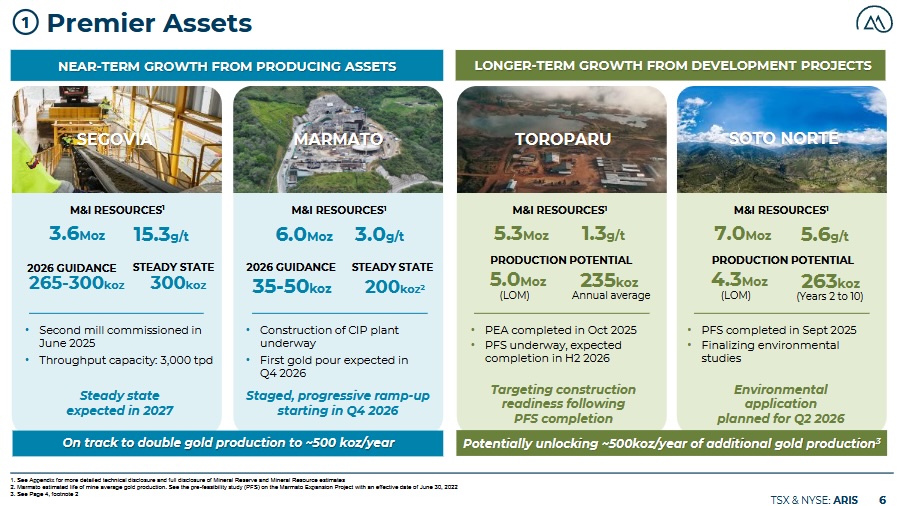

Management knows how critical their presentation is, so they condense their best data into it. Here is Aris’ slide about their mines.

Source: Aris Mining corporate presentation

As we can see, Aris owns 4 large mining projects. Segovia, Marmato, Toroparu, and Soto Norte.

The cash cow today is Segovia, located in Colombia, South America. Segovia is a very high-grade underground mine. At a headline ~15.3 grams of gold per ton of rock, this is an elite-grade mine. Here’s what it looks like in the tunnels:

Source: Resource World

In 2026 Segovia should produce 265,000 to 300,000 ounces of gold. That’s the vast majority of the company’s current production. This number includes gold the company mined itself (about 60%), as well as gold they mill for other miners at their facilities (about 40%). Margins are higher on self-mined gold, but the “contract mining partners” is a nice topper.

The company expects to reach 300,000 ounces of gold per year at Segovia. This is their mature mine.

Aris’ goal is to reach 1 million ounces of gold produced per year. That would put them in the big leagues, but will require basically 4xing current production.

That will require all 4 projects to get fully permitted and up and running. It’s a multi-year goal.

If they can get all 4 projects humming, 1 million ounces a year is attainable. But in the mining world, getting environmental approvals and permits is a huge part of the challenge.

Political Geography

In the world of mining, politics plays a big role. Getting mines permitted depends on a company’s ability to navigate labyrinths of bureaucracy and red tape.

Three out of four of Aris’ mines are in Colombia. A country rich with natural resources, but with a mixed record on friendliness to miners.

So it’s fortunate for the company that a conservative just won the presidential election. On June 21st, President-elect Abelardo De La Espriella beat Gustavo Petro in a very close race.

On August 7th, new President De La Espriella will take office. This is a very good sign for Colombian miners. The old president was not friendly to the mining industry. The new one is pro-business and more likely to encourage regulators to issue environmental permits.

Aris’ Soto Norte site is still conducting its environmental studies, and will need to get permits in order to reach the company’s 1 million ounce a year goal.

The election of a conservative president will help with this process, but it’s no guarantee.

When we buy gold miners, junior or senior, we need to consider the geography and political environment they’re operating in. Mining is a very political sector.

So far, the management team has navigated the political side of things well. Aris’ CEO and Chairman, Neil Woodyer, is a mining vet and has assembled an experienced team of operators.

More Risk, More Reward

When we buy junior miners, we take more risk. Companies at this stage will likely need to raise money, diluting existing shareholders or adding debt. In the case of Aris, they’re already generating significant cash flows, so may not have to raise again anytime soon.

But with multiple development and exploration projects, there’s endless permitting, drilling, and construction to be done. Each takes time and money.

If companies spend it well, raising money is not a problem. It’s part of the game.

If Aris pulls off their plan, the rewards should be significant. Of course, their success will also depend on the price of gold.

And just like yesterday, this article is not an endorsement of Aris. I think the company could do well, but don’t currently own it.

It’s simply a good example of a larger junior miner. One which could be an attractive target for a gold major to acquire down the road. Aris has mines with excellent grades of gold, impressive growth, experienced management, and multiple promising mines in development.

Because juniors have a higher risk profile, sometimes it’s best to buy a diversified basket like the Sprott Junior Gold Miners ETF (SGDJ). I’ve owned this fund for years and it’s done quite well.

Since the Iran war began, juniors have pulled back significantly. I don’t believe this precious metals bull market is over. So both junior and senior miners look great here. SGDJ is a nice way to play juniors.

Have a great weekend everyone.

Comments: