Goodbye to Inflation?

CNBC gives the day’s headline news:

Inflation fell to its lowest annual rate in more than two years during June, the product both of some deceleration in costs and easy comparisons against a time when price increases were running at a more-than-40-year high.

The consumer price index, which measures inflation, increased 3% from a year ago, which is the lowest level since March 2021.

Yet why? Why has inflation sunk to its lowest ebb in over two years?

Is it because the Federal Reserve has successfully wrung inflation from the economic system?

Or is it because recessionary pulls have exerted drag upon the consumer… and he has reined his spending?

Or is today’s inflation report merely an illusion, a mirage? Consider:

Energy costs have decreased some 16% since last June. This has exerted a negative gravitational pull upon the headline rate.

That is the 3% headline rate to which we were alerted today.

Core Inflation and the Fed

Meantime, the core inflation rate — the inflation rate absent food and energy components — increased 4.8% on the year-over-year time scale.

A 4.8% inflation rate is an elevated inflation rate. It is not a galloping inflation rate. Yet it is an elevated inflation rate.

And it is this rate, the core inflation rate, that the Federal Reserve monitors most — not the headline rate.

Its preferred core inflation rate is 2%. A 4.8% rate suggests the Federal Reserve is not prepared to abandon its anti-inflation combats.

Thus it will remain on the warpath.

Powell Doesn’t Want to Repeat Volcker’s Mistake

Mr. Powell is out to avoid Paul Volcker’s 40-year-old error. That is, he is reluctant to declare a triumph until inflation is well and truly scotched.

Explains Jim Rickards:

Jay Powell does not want to repeat the mistake of Paul Volcker, who also fought inflation with rate hikes, but cut rates too early and came to regret it.

When Paul Volcker was appointed Fed chair in 1979, he immediately set about ending the worst inflation the U.S. has seen since the end of World War II by raising rates.

Then the U.S. was hit with a recession in January 1980… [and] Volcker was under intense pressure to cut rates in the face of a recession and layoffs.

The Fed blinked. Volcker lowered the fed funds target rate by 7 percentage points.

The recession was over by July 1980, but inflation was not… The Fed and Volcker had damaged their credibility as inflation fighters.

This became known as the infamous Volcker Mistake…

If Volcker had ignored the 1980 recession, inflation might have come down by 1981. Instead, it lasted until 1983 and was only defeated by a recession worse than the one Volcker was initially worried about…

Jay Powell does not want to repeat the Volcker Mistake. He knows how that turned out and doesn’t want to end up in the history books for the same thing.

We hazard he does not. Will today’s inflation report influence him and his mates?

Expect a July Rate Hike

The Federal Reserve is scheduled to convene later this month.

Markets presently give 95% odds — 94.9% odds to be precise — that it will enact a 0.25% rate elevation at this convening.

“We’re not in the Promised Land of the 2% target,” says Bankrate’s Mark Hamrick, adding:

“We know the journey is progressing, but it’s not yet over.”

Mr. Robert Tipp, of PGIM Fixed Income, affirms the thesis that Powell is out to avoid the abovesaid Volcker error.

Reports Zero Hedge:

Tipp tells Bloomberg TV he is not ready to call the widely expected rate hike in July as the last. While it “feels good” to get a print like this, he said he thinks the Fed will not risk having inflation reaccelerate.

Ms. Megan Horneman, she of Verdence Capital Advisors, is in forceful agreement:

There’s still three areas of the inflation that the Fed’s looking at very closely — service inflation, wage inflation and housing inflation. All three of those things, while they are moderating, are still uncomfortably high…

Even if this print came in softer than expected, it’s not still not enough for the Fed to say their job is done. I don’t think they are going to be cutting… The market is too optimistic about the path and timing on rate cuts. We think they are going to stay higher for longer — they told us that.

Wall Street Isn’t Impressed

Perhaps the above comments explain why Wall Street’s reaction to today’s report was… subdued?

Stocks took a jump, yes — but not a rambunctious jump, not a joyous jump, not a jubilating and exhilarating jump.

The Dow Jones Industrial Average posted an 86-point advance. The S&P 500 went 33 points forward.

The Nasdaq Composite outjumped them both substantially — a 158-point leap.

Gold — meantime — did take a rambunctious jump today, a joyous jump, a jubilating and exhilarating jump.

It journeyed from $1,937.10 at opening bell to $1,963.50 by closing whistle — a $26.40 spree.

Ten-year Treasury yields slipped nearly 3% today, to 3.86%.

Merely two days prior, on July 10, yields crested at 4.08%.

That is a substantial coming-down within so short a span.

What does it portend? A further reduction in the rate of inflation? Perhaps an economic slowing-down… perhaps even recession?

We do not know.

Yet a worrying information has come drifting in over the wires…

Major Recession Warning Is Flashing Red

Reports The New York Times:

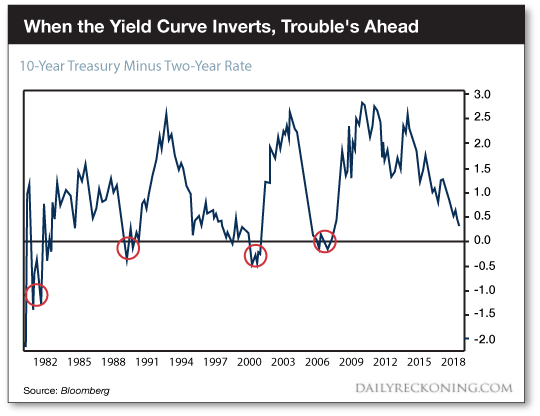

Wall Street’s recession warning is flashing… That signal, called the yield curve… is now sending its strongest warning since the early 1980s of a coming downturn… The last time the yield curve was so inverted was in the early 1980s, when the Fed battled runaway inflation, resulting in a recession.

The yield curve. We generally endeavor to avoid such economic arcana as the yield curve.

It is tedious business. Yet here is our distilled explanation, our CliffsNoted explanation:

The yield curve is simply the spread between short-term interest rates and long-term interest rates.

Long-term rates normally run higher than short-term rates. For the reasons, we needn’t look far.

Investors, for example, demand greater compensation to hold a 10-year Treasury than a 2-year Treasury.

They are, after all, locking away their money for 10 years — as opposed to two years. Would you not demand greater compensation under the 10-year option?

And the 10-year outlook is far less certain than the two-year outlook.

Thus the 10-year yield should therefore run substantially higher than the 2-year yield.

Meantime, the 10-year Treasury yield rises when markets anticipate higher growth… higher inflation… higher animal spirits.

Signs of Trouble

But when the 2-year yield and the 10-year yield begin to converge, the yield curve is said to flatten.

And a flattening yield curve is a possible omen of lean days — and lean nights.

Is a flattening yield curve an immediate menace, a thundercloud overhead?

Not necessarily, say the experts. Not necessarily.

The yield curve can stay good and flat for a long stretch — with no ill effects.

Only when the yield curve inverts do the klaxons begin to blare. Suddenly the two-year yield exceeds the 10-year yield.

That is, a man now earns greater interest through a shorter-dated two-year instrument than he earns through a longer-dated 10-year instrument.

It is a preposterous formula. It suggests a severe economic discombobulation ahead.

Here is the graphic evidence, stretching to 1980 (we omit the 2020 recession due to its “unnatural” origins):

The Loudest Recession Warning Since 1982

The yield curve technically inverted last July.

Today the 2-year Treasury note yields 4.78%. The 10-year Treasury note yields a curve-inverting 3.86%.

The spread between them equals -0.92%

That, again, is the greatest spread since 1982. Thus the Treasury market gives off the loudest recession alert since 1982.

When — then — can you expect the recessionary hammer to come lowering down?

History reveals the catastrophic effects of an inverted yield curve only manifest an average 18 months post-onset.

Countdown to Recession

Let us assume the present inversion proves no exception. The inversion predates the recession by 18 months.

Recall: The yield curve inverted last July.

We conclude the economy may peg along until… January 2024.

That is, recession comes in six months from today.

Of course we deal with averages. The blow may come landing later than January.

There is even the possibility — however diminished in our estimation — that it may never connect at all.

Yet the blow could likewise come much sooner — and from a clear sky.

Is your guard up?

Comments: