The Next Inflation Wave is Here

Inflation came in hot in April.

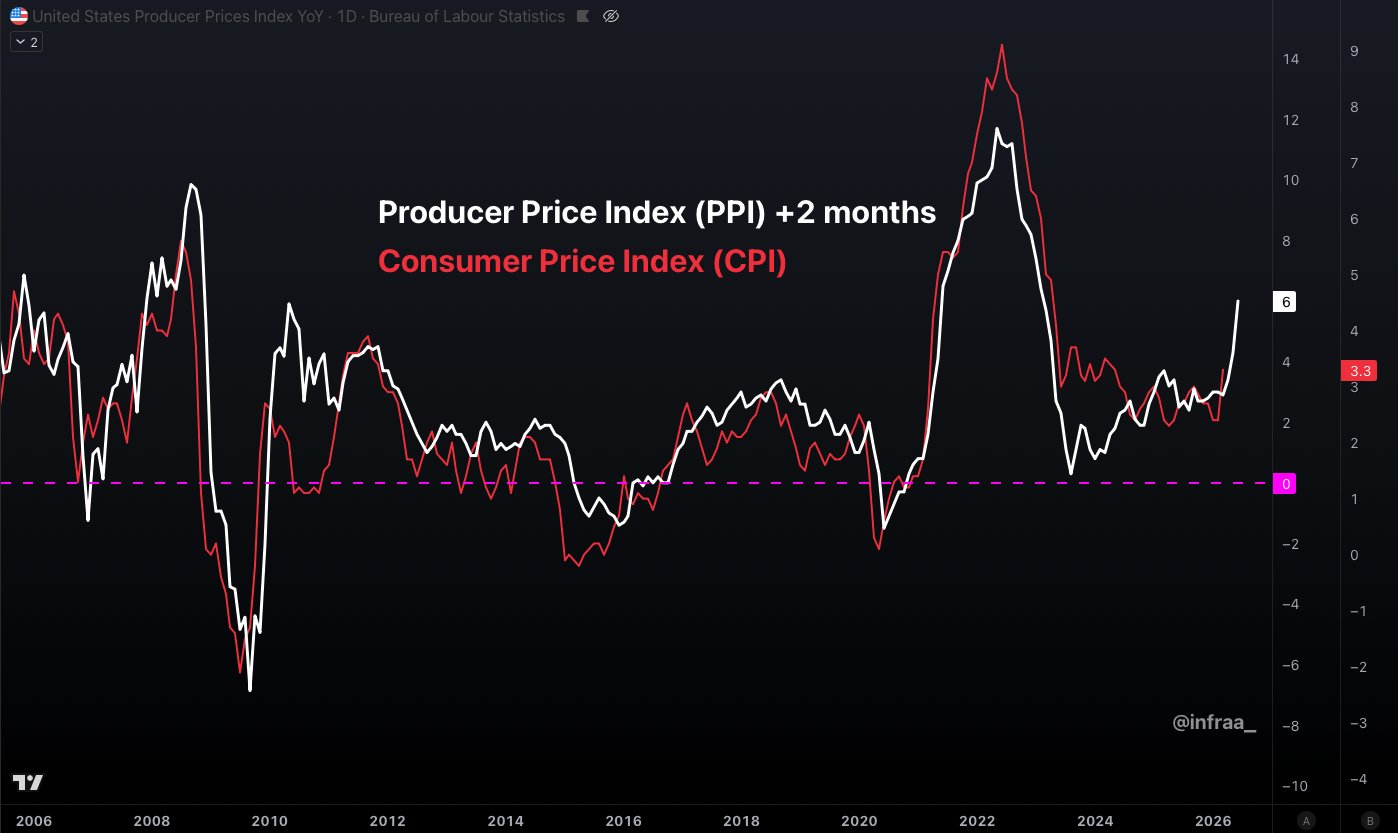

The producer price index (PPI) rose 6% year-over-year. That’s the price companies pay for wholesale goods.

The bad news is that consumer inflation (CPI) tends to follow PPI with a lag of around 2 months.

The chart below shows how closely CPI and PPI track (with PPI running 2 months ahead):

Source: Robert infra on X

Note the large spike from back in 2021 and 2022. That was related to post-COVID inflation caused by massive monetary stimulus. And of course in 2022 Russia invaded Ukraine, which compounded the problem by spiking oil and fertilizer costs.

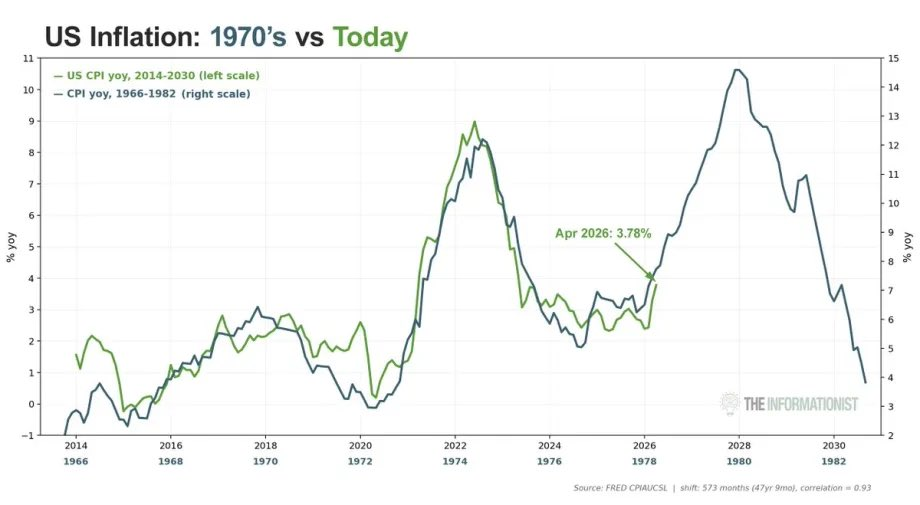

Here’s another chart showing how recent inflation trends (green) match up to the 1970s (blue):

It’s worth noting that official inflation was higher in the 1970s, peaking out at around 12% in the middle wave, and 14.5% in the final move.

Our “middle wave”, which peaked in 2022, rose to a high of around 8.5% inflation.

This is mostly due to differences in how CPI (inflation) is measured today. Now we have fancy tools like “hedonic adjustment” which make inflation appear lower than it truly is.

So in reality, we’re on a similar trajectory to the 1970s inflationary period. The primary difference is the level of debt we have today.

America’s current debt to GDP ratio is around 125%. In the 1970s it topped out around 35%. So we have 3.5x more debt today in comparison to the size of the economy.

Today’s huge debt load severely limits the Federal Reserve’s options.

To kill the 1970s inflation wave, Paul Volcker hiked to a crazy 20% fed funds rate. That is no longer an option due to the huge amount of debt we have.

Even if we see another major wave of inflation, I don’t see the Fed hiking interest rates. The math simply doesn’t work.

The Fed’s Dilemma

President Trump’s nominee, Kevin Warsh, was just confirmed by the Senate.

Tomorrow he will take over from Jerome Powell, who is considered somewhat of an inflation “hawk”, meaning he hiked interest rates to attempt to control inflation.

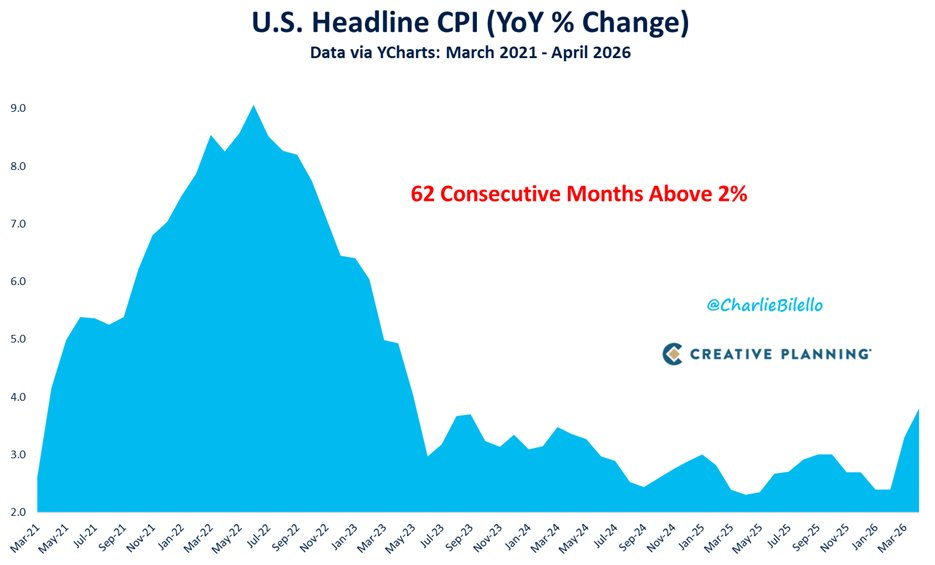

However, as the chart below shows inflation has remained above the Fed’s 2% target for 62 consecutive months.

Source: Charlie Bilello on X

President Trump has criticized Powell sharply over his refusal to cut rates further. And he’s not wrong.

Even though on paper the Fed “should” be raising interest rates, it would be extremely destructive to do so.

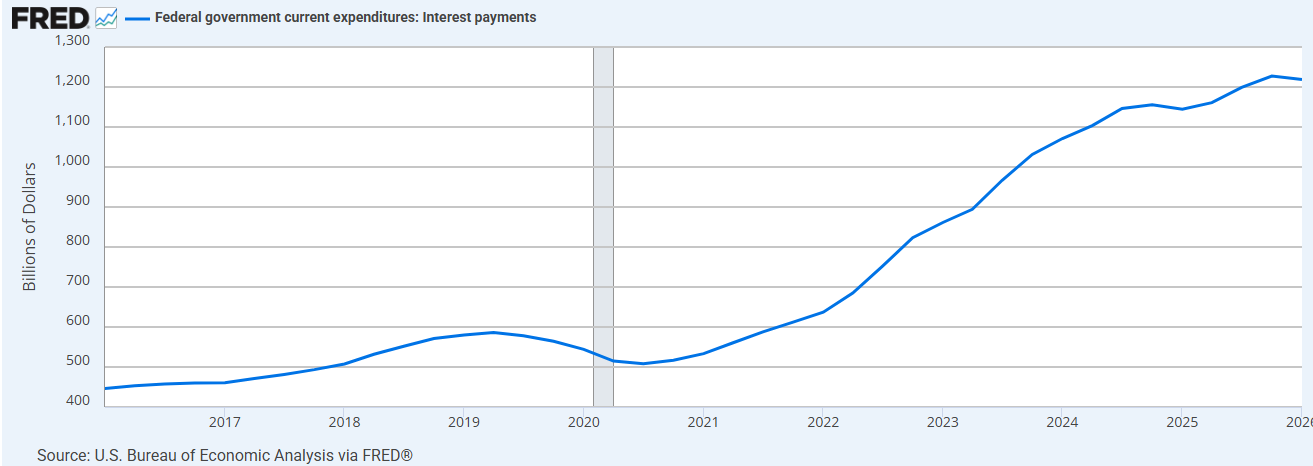

We have reached a point in this debt cycle where just paying the interest on the federal government’s debt costs $1.2 trillion per year. Here’s a 10-year chart:

Source: St. Louis Federal Reserve

In 2020, when interest rates were lowered to near-zero, interest costs got as low as $500 billion. Now that cost is $1,218 billion annualized ($1.2 trillion).

In 2025, total U.S. tax revenue was about $5.2 trillion. So 23% of taxes are being spent to pay interest on our debt. It’s outrageous.

At this point, higher interest rates would be devastating. We’d rapidly be paying $2 trillion in interest. Then things would rapidly snowball out of control.

In a perfect world the Federal Reserve is supposed to be “independent”. They are only supposed to adjust interest rates to cap inflation at 2% and keep employment high.

In the real world, they need to think about our country’s debt situation. And that means that in the mid-long term, rates need to be lower.

Financial Repression

This brings us back to the concept of “financial repression”. My belief is that the Fed will be forced to cut rates even as inflation is well-above target. They will have to buy large quantities of U.S. debt, essentially financing government excess.

Eventually they will institute “yield curve control” and keep rates artificially low, even if inflation is out of control.

I’ve been focusing on this topic so much lately for a reason. We’re approaching the point where drastic measures are going to become necessary to control the debt spiral.

Kevin Warsh will soon begin his term as Fed Chair. I believe he will go along with Trump’s wishes and cut rates, even if inflation is high.

Rate cuts may not happen immediately, but we need to start lowering this year. The debt situation is becoming urgent. And that will take precedence over inflation, as uncomfortable as it may be.

Starting as early as next year, more drastic measures will likely become necessary. Massive QE (quantitative easing), eventually leading to yield curve control.

During times of financial repression, hard assets and natural resources are key to preserving and growing wealth.

I want to own miners with huge projects that will last another 20 or 30 years. I want to own the best oil producers with billions of barrels of oil in the ground. Companies with real assets that will grow in value no matter how crazy things get.

We will continue to explore ideas to help readers navigate the coming storm.

Comments: