My Favorite Way to Play Gold’s Rise

The past few years have been unusual for gold and interest rates.

Both have ripped higher together.

Historically, these two are often inversely correlated, meaning when the bond yields are high, gold is weak. And vice versa. But no longer.

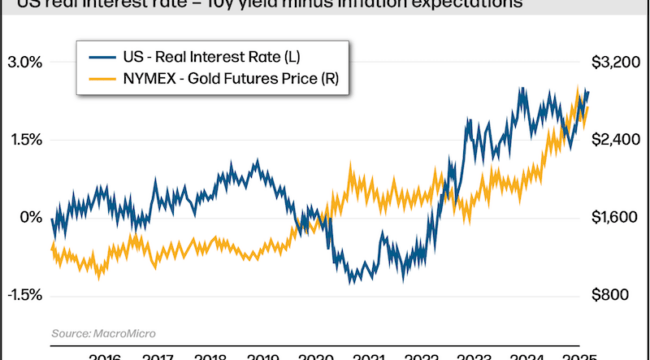

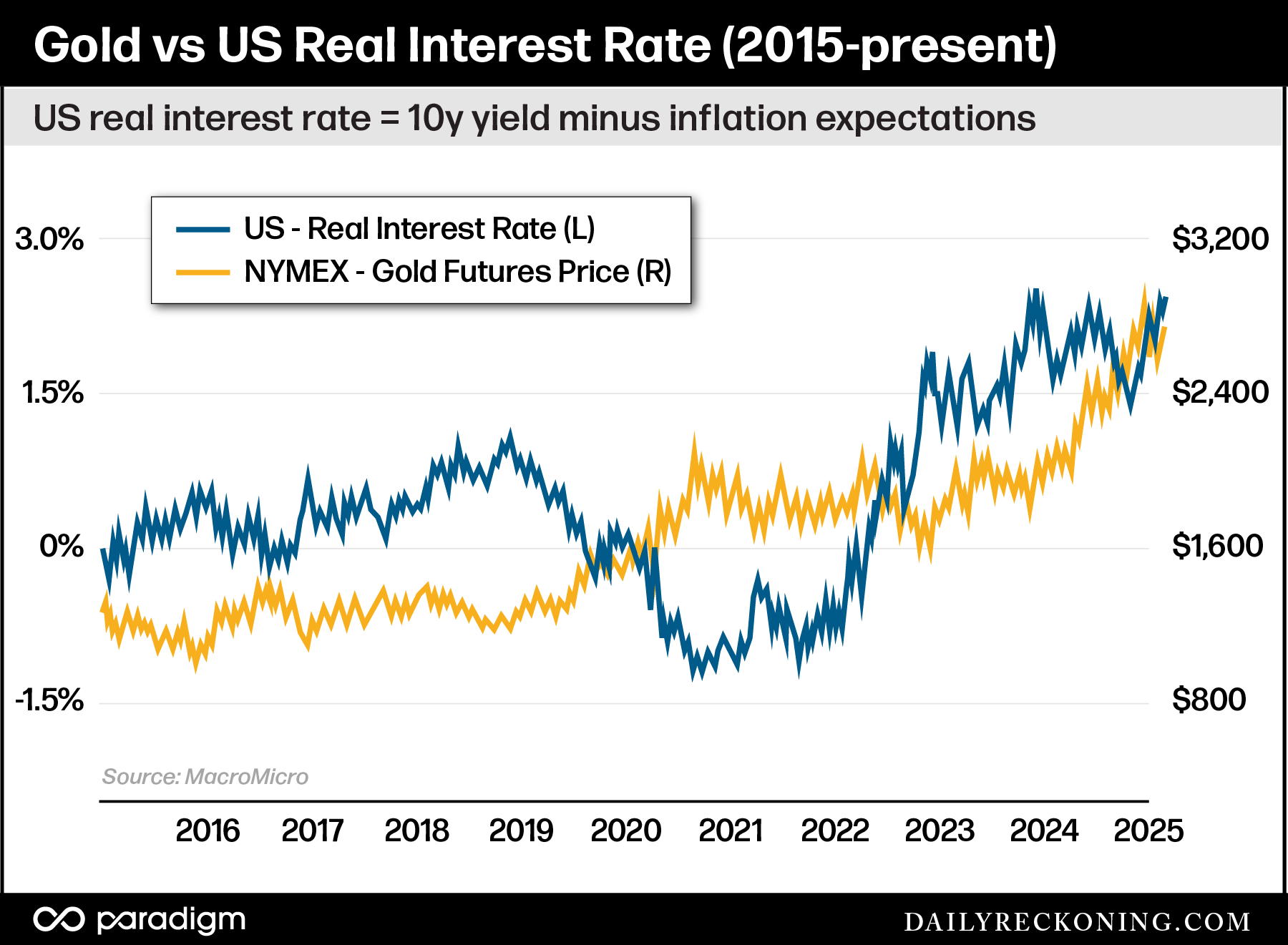

The chart below shows the price of gold vs. U.S. real interest rates (10y bond yield minus inflation expectations):

As you can see, the two traded inversely up until 2022. When yields rose, gold fell. When yields fell, gold rose.

The old paradigm made sense. When real yields on bonds are high, more investors will switch out of gold and into Treasuries. When yields are low, gold becomes more attractive as a way to preserve purchasing power.

So why did this relationship change beginning in 2022?

Well, there was that minor incident where the U.S. confiscated $300 billion of Russian central bank assets. Remember that? It was part of Uncle Sam’s punishment package after Russia invaded Ukraine.

Surely that couldn’t be related. Right?

Direct Consequence

My colleague Jim Rickards has been all over this story. Back in October of last year, he penned a piece titled This Will Destroy the Dollar.

For context, this was just after Treasury Secretary Yellen had accused Trump of being a threat to America’s financial system.

Here’s an excerpt:

The irony is that Yellen herself is the greatest threat to the Treasury market through her persistent and illegal efforts to steal $300 billion in U.S. Treasury securities owned by the Central Bank of Russia and held in custody in U.S. and European banks and the Euroclear clearinghouse in Brussels.

That particular threat to steal the Russian securities to be used as backing for a loan to Ukraine has accelerated efforts of the BRICS and the Global South to move toward a new currency linked to gold that would initially compete with the dollar in global payments and eventually rival the dollar as a major global reserve currency.

So yes, the Biden admin’s move to confiscate Russian assets played a primary role in breaking the traditional relationship between gold and real rates.

It worked twofold. First, it naturally increased demand for gold from central banks, as we have covered extensively. Ever since, central bankers have developed an unquenchable thirst for gold.

Gold is apolitical. As long as it’s in a vault within a country’s own borders, there’s really no safer asset one can own. It is the ultimate sovereign form of money.

As a result, the price of gold is up more than 40% since Russia’s invasion and the subsequent confiscations and sanctions. 2022 marked a turning point in central bank reserve policies all over the world.

I believe central bankers will continue with their rebalancing away from U.S. bonds, and towards precious metals. While a few dedicated countries have been adding to their gold reserves, many are still severely underinvested in this area.

Secondly, the confiscation decreased foreign demand for Treasury bonds. If the government hadn’t confiscated Russia’s assets, I’m sure that foreign demand for U.S. Treasuries would have soared as interest rates rose.

But even with far higher yields, foreign demand for American bonds has been tepid. This has accelerated the convergence between gold and real rates.

Trump’s Difficult Choices

When Trump enters office, greeting him will be a huge pile of bad decisions and mistakes made by the Biden administration.

Chief among them is the confiscation of Russia’ $300 billion. Trump is in a tough spot here. If he returns the money to Russia, his opponents will undoubtedly scream that he’s a tool of Putin.

If he doesn’t return the money, U.S. Treasuries will continue to decline in popularity among central banks.

Either way, the Biden admin already opened Pandora’s Box. Every central banker in the world now knows that certain risks apply to their U.S. assets.

As a result, I don’t think the Treasury market will ever fully regain its primacy. Trump certainly has a chance to slow the decline, but to reverse it would be a herculean task.

The world is finally moving towards making gold a primary reserve asset once again. Central bank buying should provide an excellent floor on prices going forward.

As investors, our takeaway should be simple: buy and hold gold. Physical bullion is always a great option. In terms of ETFs, I like the Sprott Physical Gold Trust (PHYS).

Comments: