Is the Fed Blowing the Biggest Bubble in History?

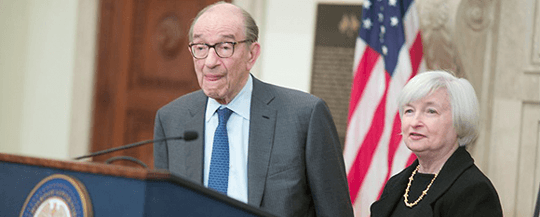

Before the Fed’s policy committee meeting in September 1996, then Chairman Alan Greenspan received a special visitor in his office…

His guest was a relatively new and little-known Fed governor with a bone to pick with him.

She thought the Fed chief was being reckless by not raising interest rates.

And she implored him to do so at the next Fed meeting or risk losing her support.

But she wasn’t prepared for what happened next…

This Time Is Different

That little-known Fed governor some 20 years ago was Janet Yellen.

She and her colleague, then Federal Reserve Board Governor Laurence Meyer, requested a special sit down with Greenspan because they thought the economy was in danger.

Here’s how Meyer described it:

“Janet and I were both worried about inflation, even though it was very well contained at the time. We told the chairman that we loved him but could not remain at his side much longer if he continued, as he had been doing for some time, to push the next tightening action into the next meeting, and then not follow through.”

With unemployment low at roughly 5%, Yellen thought it was past time to raise rates.

But Greenspan pushed back unexpectedly. He knew better.

You see, he said this time was different…

Back then, Greenspan was preaching the unique benefits of the “new economy” and technology-driven productivity growth.

He thought productivity was increasing more than was being recorded, so the rate of inflation was overstated.

So the Fed needed a new approach. Greenspan saw little risk from inflation and wanted to keep interest rates low.

And that’s just what he did, keeping rates too low for too long. That helped create the stratospheric rise in stock prices as the “new economy” market bubble inflated in the late 1990s and then imploded in 2000.

The Fed raised interest rates six times between June 1999 and May 2000 to try to make up for its mistake. But it was too late.

Greenspan played with rates again a few years later. It was different then too. This time it was the false fear of deflation.

To fight it, Greenspan lowered the Fed funds rate to a record low of 1% in July 2003… and he kept it there for a year.

Keeping rates too low for too long again pumped up the biggest real estate bubble in U.S. history—which popped in 2008.

To repair the damage and raise stocks and real estate yet again, we all know what flowed next—the alphabet soup of QE, ZIRP, etc.

The Master Bubble Blower

Now fast forward to 2016, and it’s clear that Yellen learned a lesson from her meeting with Greenspan… but it’s not the one you’d have hoped.

Today, Yellen finds herself in his shoes…

Some Fed colleagues are pushing for higher rates… just as she did 20 years ago.

Unemployment has been at or under 5% for more than a year.

And the U.S. inflation rate hit a nearly two-year high in September.

The Janet Yellen of 1996 would have argued forcefully for a rate hike long ago.

But like Greenspan, the Yellen of 2016 knows better. This time is different… again.

After 8 years of near-zero rates, and effective negative rates due to inflation, she says we need a “high-pressure economy” to fix the unique economic damage done during the Great Recession.

Once again, the Fed needs a new approach in order to keep interest rates low.

Sure, a December rate hike may be on the table to keep whatever shred of credibility the Fed has left.

But anyone planning on an orderly procession of periodic rate hikes after that to achieve normalization is delusional.

The sober, responsible Janet Yellen who argued passionately for higher rates at 5% unemployment in 1996 is dead and buried.

Now she has the responsibility of being in charge. So she’s going to keep the punch bowl filled and let the keg party rage on her watch… just like Greenspan.

That means she’ll continue to be creative with excuses to keep rates low and asset prices fully inflated, threatening to create the biggest market bubble we’ve ever seen.

After all, she learned from a master. Alan Greenspan was a bubble blower extraordinaire. And Janet Yellen was his prized student.

But when the next bubble pops, the Fed won’t be able to raise asset prices yet again because the bullets will have left the chamber.

At that moment, we will officially be Japan—no more stock market wealth effect to trick investors into believing they are rich. The jig will be up.

Please send your comments to me at coveluncensored@agorafinancial.com. Let me know what you think of today’s issue.

Regards,

Michael Covel

for The Daily Reckoning

Ed. Note: Sign up for a FREE subscription to The Daily Reckoning, and you’ll receive regular insights for specific profit opportunities. By taking advantage now, you’re ensuring that you’ll be set up for updates and issues in the future. It’s FREE.

Comments: