Druckenmiller’s -$3B FOMO Moment

By 1999, Stan Druckenmiller was already a legend.

From 1981 to 2000, his hedge funds had never had a losing year.

His returns averaged a crazy 30% per year. Druck caught the attention of George Soros and was soon running the legendary Quantum hedge fund.

In 1999, Druckenmiller saw the internet bubble forming and built up a $200 million short on tech stocks.

But the bubble kept inflating. Soon he was down $600 million on the short position.

So Druck hired two tech “gunslingers”, and gave them some money to manage. They bought all the hot stocks and were soon making 3% a day.

The young tech bros were making their boss look like a dinosaur.

Druckenmiller describes how the FOMO (fear of missing out) seized him:

“So like around March [of 2000] I could feel it coming. I just — I had to play. I couldn’t help myself. And three times the same week I pick up a phone — don’t do it. Don’t do it. Anyway, I pick up the phone finally.

I think I missed the top by an hour. I bought $6 billion worth of tech stocks, and in six weeks I had left Soros and I had lost $3 billion in that one play.”

Let’s pause for a second and reflect. One of the greatest investors in history bought the tippy-top of the dotcom bubble. And took a $3 billion loss.

Druckenmiller has since said that he already knew it was a bad idea, but simply couldn’t resist.

“I didn’t learn anything. I already knew that I wasn’t supposed to do that… I was just an emotional basketcase and I couldn’t help myself.”

This is the power and danger of FOMO. Watching stocks go up can cause us to do irrational things.

Berkshire’s $397B Cash Hoard

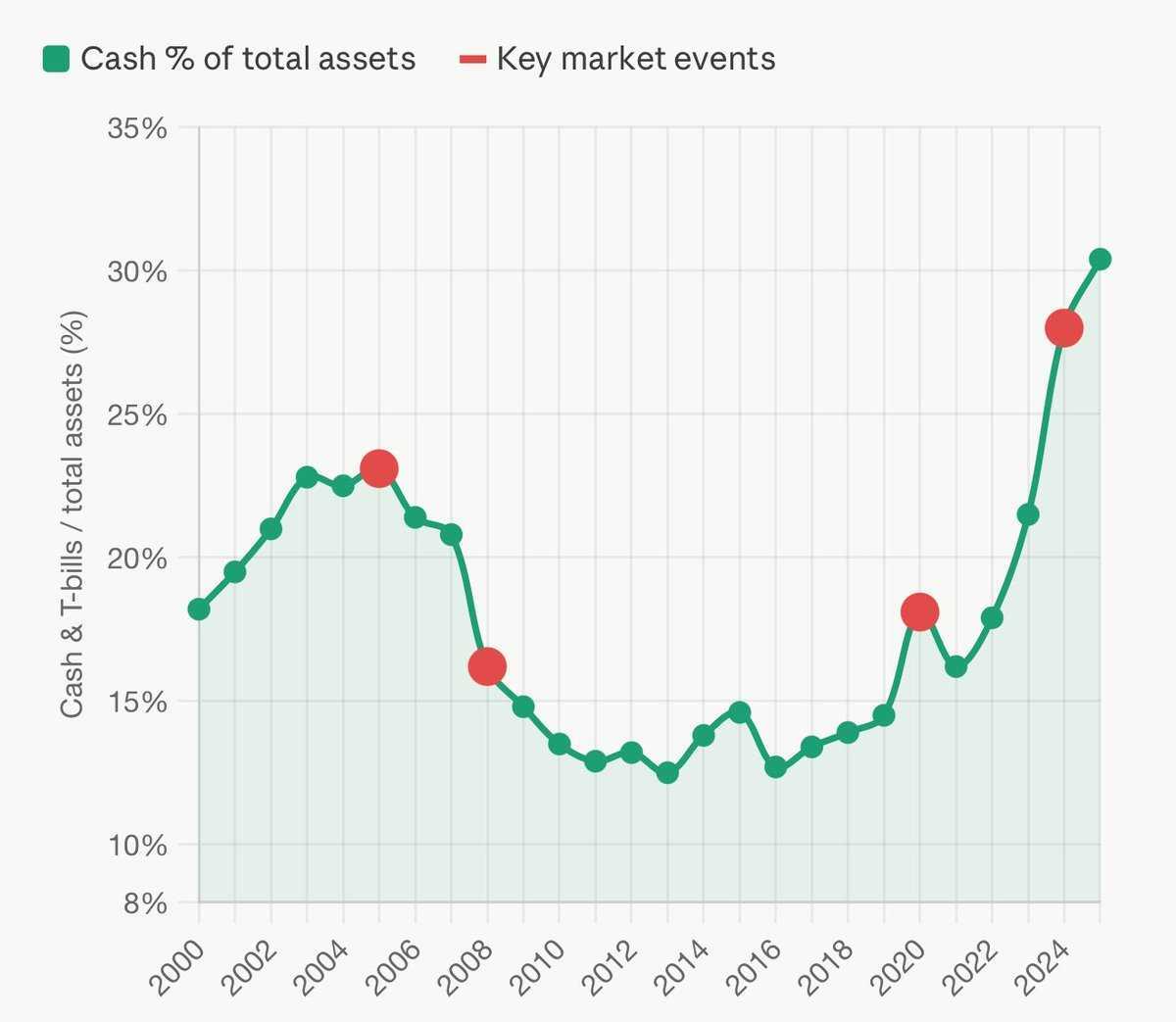

Berkshire Hathaway (BRK.A, BRK.B), the famous firm founded by Warren Buffett, is sitting on a record $397 billion in cash and Treasury bills.

That’s almost a third of Berkshire’s assets. Capital that’s only earning 3-4%, while the market rockets higher. The S&P 500 jumped 10% in April alone, during one of the most serious energy crises in history. This is clearly not a logical market.

But Berkshire is standing firm. They are patiently waiting for “fat pitches”. In other words, they’re waiting for a crash and much cheaper stocks.

The conglomerate did something similar before the 2008 crash. Their cash reached 23% before the crisis set in.

So when those juicy pitches finally came, they had cash to spend. Berkshire famously invested in Goldman Sachs (GS) at a time when bank confidence was shaky.

Buffett bought $5 billion in preferred stock with a perpetual 10% dividend. And they got warrants to buy $5 billion in stock at $115 a share. Goldman Sachs trades at $917 today.

Berkshire’s best investment during the crisis was Bank of America (BAC). That “blood in the streets” investment returned an impressive $20 billion.

Buffett and team also bought GE, Dow Chemical, and many other stocks at bargain basement prices during the crash.

It was a lesson in patience and waiting for great opportunities.

However, Warren Buffett has intentionally limited his choices. He refuses to look at emerging market stocks, and hates precious metals.

So while it is good to keep some cash around, we don’t have to sit on 32% like Berkshire Hathaway.

Assets With Less Downside, Huge Upside

Before we get into it, I want to make one thing clear. What I’m talking about here applies to long-term investments. If you’re just in hot stocks for a trade, that’s fine.

But the long-term portion of my portfolio is invested in stocks that will weather the coming storm. Natural resources, emerging markets, precious metals. And I think most people should have more exposure to these sectors.

When the crash hits, you don’t want to be overweight the most crowded sectors. When it happens, the exit door will be very small, and millions will be rushing through it.

For example, from 2000 to 2002, the Nasdaq fell 78% peak to trough. The S&P 500 fell about 49%.

During that same period, oil stocks gained around 20%, plus dividends. Gold miners did even better, with the NYSE Arca Gold BUGS Index rising more than 100% from 2000 to 2002.

And these natural resource stocks continued to outperform for another 8 years.

Emerging markets also crushed the S&P 500 and Nasdaq during the dotcom crash. The MSCI EM index only fell around 25% during the crash, quickly rebounded, and outperformed U.S. stocks for years to come.

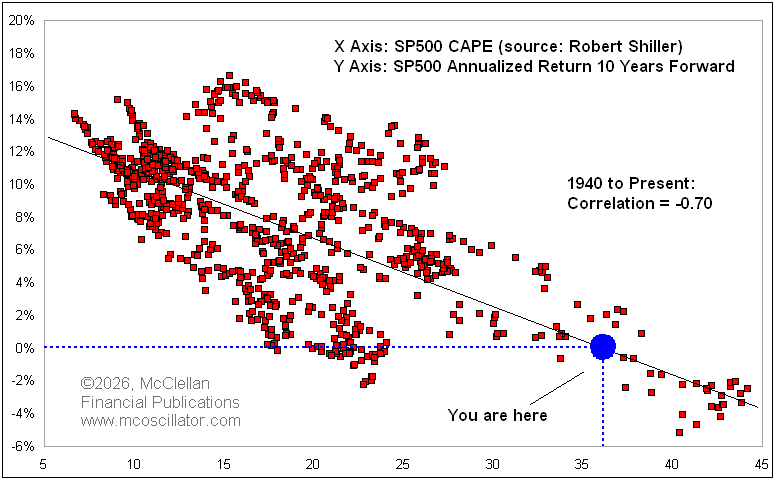

The point is simple. U.S. stocks are very expensive today. Historically when this has happened, forward returns have been very low.

The chart below shows the CAPE ratio (a 10-year measure of how expensive stocks are) of the S&P 500 (x-axis) and the annualized returns which followed (y-axis).

Based on today’s CAPE ratio (around 36), returns have averaged around 0% over the next 10 years.

Source: Tom McClellan

Sure, the S&P 500 could rocket up another 15%, but that would likely signal a “blow-off” top. There will be a crash at some point. And following that crash, we don’t know how long it will take overpriced stocks to recover. After the 2000 dotcom bubble bust, it took over a decade.

I’m not saying to go out and sell all your pricey stocks. What I’m recommending is diversifying into alternative investments. Natural resources, emerging markets, and precious metals.

Eventually, the time will come to sell these unusual assets, and shift into more traditional growth and income stocks.

But that time will only arrive when yields on “normal” U.S. stocks are much higher, and prices are much lower.

Just to reiterate – this applies to long-term investing. For quick trades, buying overpriced stocks can be profitable. Just be sure to manage your risk appropriately.

Comments: