Why Interest Rates Won’t Return to Zero

Many observers expect interest rates to fall back to zero as inflation dissipates and central banks rush to stimulate flagging economies. This expectation is reasonable based on the events of the past 15 years (2008–2023), but if we zoom out to a 50-year timeline, we get a different perspective and draw a different conclusion.

2023 is not 2008, and the difference can be summed up in one phrase: Global risk has been repriced.

Interest rates reflect not just inflation expectations and central bank stimulus; interest rates and bond yields also reflect the risk premium on the cost of credit-money, and if the risk profile has changed in fundamental ways, the risk premium and cost of credit-money will reflect that, regardless of inflation and central bank stimulus.

The global economy is changing in fundamental ways, and this is repricing everything: the cost of money/credit, the price of assets, the value of hedges and insurance, and so on. The core driver in all this repricing is risk, for it’s the reappraisal of risk that forces the repricing of everything.

When risk is low and transparent, the risk premium is low and this is reflected in low, stable costs. When risk soars and is difficult to assess, the risk premium rises and this pushes costs higher.

In terms of asset valuations, higher risks reprice assets higher or lower based on the risk profile: what happens to the asset if liquidity dries up in a risk-driven crisis? If credit dries up, what happens to demand for the asset?

Risk tends to be self-reinforcing. If we look around and see everyone else is confident that risk is theoretical rather than real, we stop buying hedges against bad things happening, and we pay a premium for assets that do well in low-risk eras.

But if we see other people getting defensive — selling assets, paying down debt, reducing spending and risk-on investing–then we pull in our horns, too.

What changed? The global economy began a cycle in the early 1990s of declining risk throughout the system due to these risk-reducing changes:

1. The dissolution of the USSR and the end of the hyper-expensive, heightened-risk Cold War.

2. The flood of low-cost oil as all the super-giant fields discovered in the 1970s began peak production.

3. China emerged as the low-cost “workshop of the world,” enabling 30 years of soaring corporate profits as corporations reduced costs by offshoring production to China.

4. This offshoring boosted profits while deflating the costs of production due to much lower labor costs, lax / non-existent environmental standards and Chinese producers’ willingness to accept razor-thin profit margins.

5. The reduction in global risk and the deflationary impact of Globalization (offshoring and opening new markets) enabled central banks to lower interest rates for 30 years without sparking inflation and private-sector banking/lending to expand credit and leverage, effectively globalizing /commoditizing financial instruments that hedged risks (Financialization).

6. After a decade-long lag (the 1980s), the advances in personal computing, software and desktop publishing finally began generating productivity increases.

7. The economic theology of Neoliberalism was embraced globally. Neoliberalism claims “markets solve all problems” and so the universal solution is to turn everything into a market by reducing regulations and state oversight.

All of these forces tended to restrain prices of commodities, goods and services and reduce systemic risks while expanding markets, financial “innovations” and profits. This created a global “virtuous cycle” in which each dynamic reinforced the others.

This “virtuous cycle” ended in the 2008-09 Global Financial Meltdown, but was papered over for a decade by extreme policies:

1. China launched the largest credit expansion in history (Russell Napier’s phrase) to counter the meltdown.

2. The Federal Reserve and other central banks began a policy of financial repression (i.e. centrally managing financial markets rather than let market forces dictate liquidity, price, risk, etc.), leading to Zero Interest Rate Policy (ZIRP) that was effectively negative-rates since inflation continued sputtering along at 1.5% to 2%.

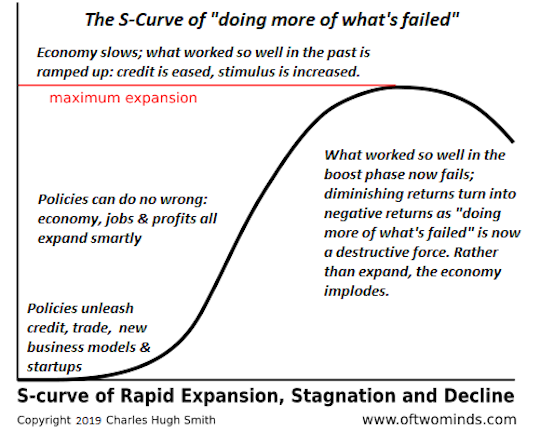

Why did the “virtuous cycle” end? The basic answer is diminishing returns: the returns on any new policy or dynamic such as Neoliberalism, globalization or financialization follow an S-Curve (see chart below), where the initial returns are stupendous (the boost phase) and then as the dynamics become ubiquitous, the returns diminish until they stagnate.

At that point, the system decays unless new more extreme measures are applied–for example, China’s debt to GDP ratio doubling from 140% to 280% and interest rates being suppressed to zero.

Another factor is the cannibalization of domestic markets once globalization had skimmed the easy returns. Financialization starts out looking “innovative” by claiming it can hedge all risks at low cost, effectively lowering the risk of playing financial games to zero. As Benoit Mandelbrot and others have explained, this isn’t possible for structural/mathematical reasons (markets are fractals, etc.).

As the easy gains diminish, financialization takes assets that were once low-risk and commoditizes them into “instruments” that can be sold globally as “low-risk assets.” This is what happened to home mortgages, which went from being highly regulated and low-risk to being poorly regulated/fraudulent and packaged into highly deceptive mortgage-backed securities that masked the true risk — high — behind flim-flam claims of low risk.

Suppressing the cost of capital/credit to near-zero generated a tsunami wave of private-generated capital, both within the banking sector and the ballooning non-banking (shadow banking) sectors. This low-cost credit was then unleashed into global markets to chase any high-yield investment, which of course means gambling on risky assets while supposedly hedging the bets against losses.

All this financial engineering — ZIRP, cheap, abundant credit, the chase for yield — ultimately depends on liquidity, i.e. the presence of buyers in size to create a market for anyone who seeks to sell an asset. If liquidity dries up for whatever reason — a bank crisis, a market panic, etc. — then sellers run out of buyers and the market reprices the asset at lower and lower levels until buyers emerge. In a bidless/zero-liquidity market, there are no buyers at all until the price approaches zero.

The potential wipeout of bubble-generated “wealth” would bring down the entire global financial system, for all those assets are collateral for the world’s immense mountain of credit/debt.

What changed around 2007-09? Globalization and Financialization moved from “virtuous cycle” to stagnation/decline, policies became more extreme to mask rising systemic risks, and the addition of a billion new workers aspiring to all the commodity-consuming luxuries of the middle class lifestyle soaked up excess production of oil and other commodities. With surpluses gone, prices had to start rising.

Post-Covid lockdown and recovery, China’s policies changed from “open to the world” and “peaceful rise” to aggressive militarization and the restriction of Chinese society’s access to the outside world.

All of these factors exposed the risks that had been successfully masked: the risks that global supply chains can break down or be disrupted by geopolitics; the risk that financialization games can blow up; the risks that soaring debt outpaces expansion of the real-world economy, generating debt crises, and the risks of extreme policies generating unintended consequences (moral hazard, extreme risk-taking, etc.) and blowback (re-industrialization, trade wars, etc.).

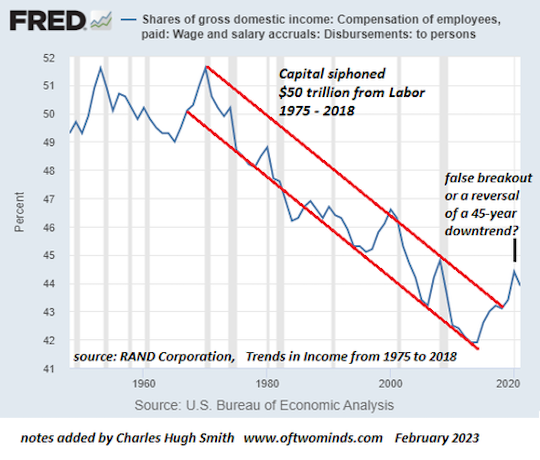

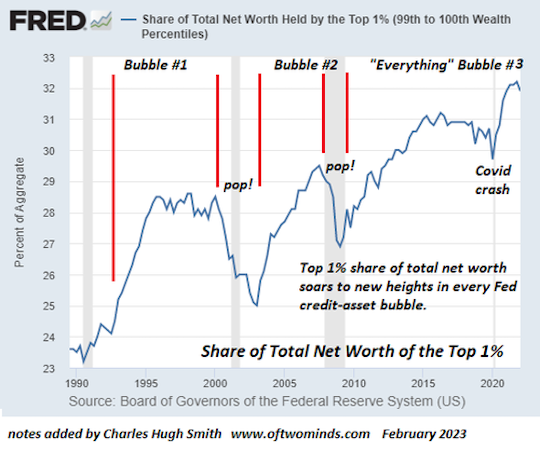

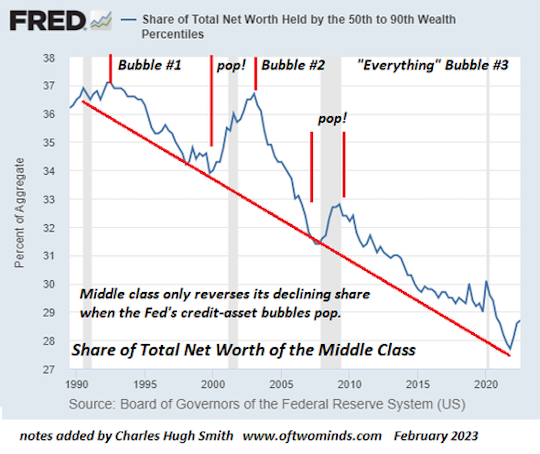

The policy extremes of ZIRP, moral hazard, credit expansion and the chasing of yields has inflated The Everything Bubble which has put the price of housing and vehicles out of reach of the bottom 60% (or in many regions, the bottom 80%) of households.

The top 5% have garnered the vast majority of the gains in asset appreciation, capital gains and profits. This generates a background of rising risk of social disorder.

On top of all this, 30 years of moderate inflation have reversed into an era of sustained inflation, which despite the hopes of many commentators, will not be transitory. This era of inflation is driven by:

1. Excessive debt levels that can only be managed by inflating the debt down to manageable levels.

2. Scarcities of essentials which push prices above what consumers can afford while not being high enough to fund massive new investments needed to increase supply.

3. The cost of capital must rise to reflect the rising risk premium globally.

All the tricks deployed to restore confidence in 2008-09 have reached such extremes that now systemic risk — of default, conflicts, broken supply chains, geopolitical blackmail, scarcities of essential commodities and perhaps the least understood risk, the evaporation of liquidity as credit and buyers of risk-on assets become scarce — is rising dramatically.

These risks are difficult to assess or hedge completely, and the inter-dependence of the global economy and financial system — a tightly bound system — means risk in one area quickly spreads to the rest of the system.

It’s clear the global risk premium has increased dramatically and is increasing in an unpredictable arc. This structural trend of higher risks will reprice everything — including bond yields and interest rates.

Comments: