The Real Inflation Number

What’s happening with inflation?

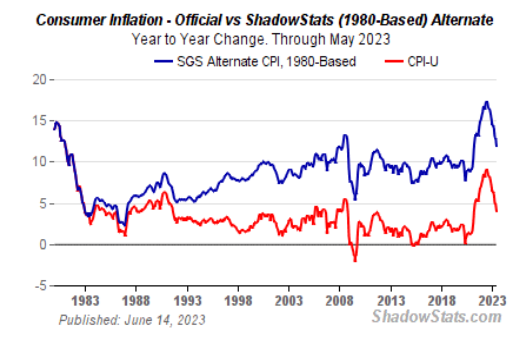

Allegedly, it’s back down in the 3.5% range, give or take; and to do it right one must give and take quite a bit. That is, again, the government number jockeys shamelessly cook the books, as we see from reviewing a site like ShadowStats.com.

Source: Shadowstats.com

If the government used the same methodology today as it used back in, say, 1980, we’d see a much higher rate of inflation. Instead of the advertised 3.5%, it might be more like 12%. And if you do things like buy a house, rent an apartment, buy a new car, pay insurance premiums, enjoy a top-shelf cut of meat from the grocery store, etc.?

Well, you know what I mean. There’s plenty of sticker shock out there, awaiting the unwary shopper. Still, prices for some things are stable, if not declining.

Yes, the cost of car insurance is soaring, but the price of gasoline in your car is down at least a bit over the past two years. And crude oil, for example, sells at around $70 per barrel, which is a source of relief at the pump; although you may also have noticed that lower-cost petroleum somehow doesn’t seem to translate into cheaper airline tickets if you travel much and track those eye-popping prices.

Meanwhile, prices for many other goods actually are falling appreciably. Look at, say, consumer electronics like new laptop computers (one of which I just bought at a remarkably low number), or a large-screen television set, and much more.

But consider where these electronic devices are made…

Those super-duper bargains on American shelves represent hard times in Asia. There, cutthroat competition and a general recession have forced companies and workers to scramble for every sliver of business and market share they can find. Many Asian firms are selling products at below production cost, just to keep the factories humming and avoid closure issues. Sure, it’s nice to have cheaper oil and low-cost electronics, but that’s not the be-all and end-all of growing the American economy. So, let’s move closer to home, where in Washington, D.C., the Federal Reserve still hints towards rate cuts.

You likely recall that the Fed cut rates this past September, an event that was widely celebrated.

But then, curiously, long-term rates actually rose across broader markets. Clearly, there’s a disconnect between what the Fed PhDs want to accomplish, and what market makers and price discovery players foresee. In other words, many smart investors believe that inflation is not yet licked.

For many decades the Fed’s target rate for inflation has been 2%, although it’s difficult to fine-tune such things. Right now, inflation is well over that level, whether you take the government’s 3.5% number or the much higher ShadowStats calculation. And yet, again, the Fed is still cutting rates.

At the other end of the monetary spectrum, central banks across the world have bought gold in large amounts, certainly over the past two years. Part of it reflects seismic-level geopolitical competition, such as we have with fast-rising China where government, businesses and individuals all buy as much gold as they can find in dollars and yuan to pay for it.

Another angle is the global trend towards de-dollarization, and this is based on widespread foreign concerns over U.S. sanctions against governments, companies, banks and individuals who step out of line with Washington policymakers.

The most illustrative element of this point about sanctions is that, if the U.S. will sanction even nuclear-armed Russia, what chance do any other countries have?

Well, they simply keep their figurative mouth shut, exercise prudent self-interest, and default to buying gold with their dollar surpluses. Hence, despite a strengthening dollar, we have the yellow metal trading at around $2,700 per ounce.

Comments: