The High Cost of Cheap Money

The stars were once again in their courses yesterday… oil was poured upon troubled waters… the dip was bought.

All was peace.

Following Monday’s sharp unpleasantness, the stock market went trampolining back.

Yet gravity reasserted itself today.

The Dow Jones Industrial Average fell 234 points earthward.

With it came the S&P 500 and Nasdaq Composite.

The first dropped 40 points. The second, 171.

Yet a question arises:

What explains Monday’s severities? Why did a Japanese sneeze give the world a 24-hour influenza?

And can you expect a relapse? Today we take up an inquiry.

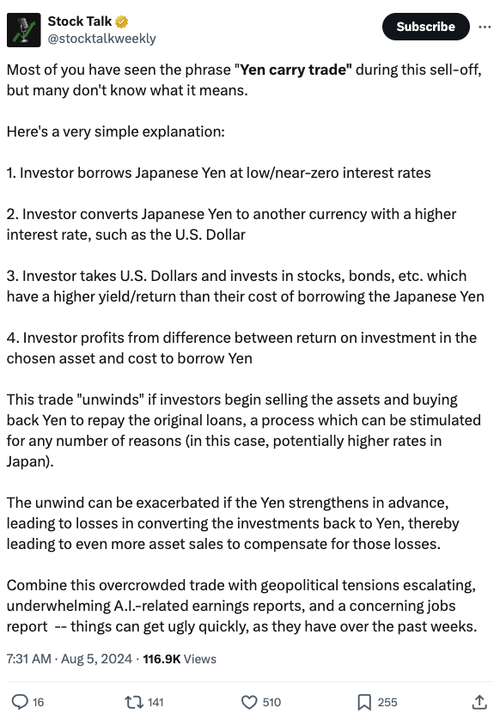

Look to the “Carry Trade”

We begin with the “carry trade,” so-called.

What is it? And how did it carry over to global markets Monday? Stock Talk:

Thus the sweet cherry — yen — becomes the hot potato.

More Lucrative Than the S&P!

Bloomberg columnist John Authers notes the following:

Since 2000 the yen-peso carry trade has yielded more juice than the Standard & Poor’s 500.

And the Standard & Poor’s 500 has yielded tubs of juice.

Yet this year the Bank of Japan put a kink in the hose.

Inflation has been on the jump and the Bank of Japan sought to choke it off some.

In March — for the first time in 17 years — Japan’s central bank imposed an interest rate increase.

Last week it imposed a second. It was a modest increase of 25 basis points. It was an increase nonetheless.

And it shook the world.

Early Monday Japan’s Nikkei index absorbed a 12% whaling.

It then fanned into existence a nearly perfect global typhoon… assaulting each corner of Earth at electronic velocities.

“This Is Where It Gets Messy”

Reports CNN Business:

Meanwhile, the dollar weakened as the Federal Reserve strongly hinted at looming rate cuts, and U.S tech stocks declined. If you’re a carry trader, you headed for the exits. But so did everyone else.

This is where it gets messy…

The carry trade relies on borrowing, which means it’s a leveraged position. (As a general rule, whenever you hear of leverage in finance, think “high risk”).

Once even minor losses start to accrue, lenders are going to demand that you pony up more cash to cover your potential losses, a process known as a margin call. That may mean selling stocks to raise cash, or closing out the position completely.

“Not everybody will have a margin call at once, but the riskiest people might, and then they start to liquidate,” John Sedunov, a finance professor at the Villanova School of Business said. “And then that creates losses for people down the chain, and then they have to sell things, and then it’s just this kind of spiral.”

In today’s interlocking markets the foot bone is connected to the thigh bone is connected to the hip bone is connected to the backbone.

Before a fellow knows what has struck him, a rumpus in his foot bone has his backbone in siege.

This we witnessed on Monday.

Asia, Europe, the United States and more endured a mighty yet brief backache.

Is the ache over? Or are we in for a relapse?

Not Done by “Any Stretch”

“We are not done by any stretch,” warns Arindam Sandilya, co-director of JPMorgan Chase’s global foreign exchange strategy.

“The carry trade unwind… is somewhere between 50–60% complete,” he adds.

TS Lombard, meantime, says:

Our analysis of past volatility bouts shows that equities take four–five weeks, on average, before a sustained recovery begins. Markets tend to rebound on oversold conditions such as the current ones, but investors often sell into that strength, which can lead to a relapse. This is what happened, for instance, in 2018, an episode that bears strong similarities to the current one.

We may not have our answer — in this telling — for four–five weeks.

Goldman’s crackerjacks tremble that “we are not going down because of recession but because of an unwind of circa 20 trillion carry trades.

“Only BOJ can stop this,” they add.

The Bank of Japan Picks Its Poison

Poor Japan. Poor, poor Japan.

It has squirmed itself into a lovely pickle jar.

It has engorged itself upon cheap money for so long… it cannot even withstand a pinprick interest rate increase against inflation… without harpooning global markets.

Its debt-to-GDP ratio comes in at a cosmic 265% or some such.

Any ratio above 90%, research indicates, swamps an economy. It cannot much expand.

Imagine then a 265% ratio.

As events stand presently, Japan must gulp poison one — inflation — or poison two: global market collapse.

On Monday poison one went down the gullet. The Bank of Japan chose inflation.

Bank of Japan Deputy Governor Shinichi Uchida pledged to refrain from additional hikings while markets remain unstable.

Yet last week’s hiking was itself the mother of the instability.

How then can he hike again?

Here is the short answer: He cannot. Do you prefer the long answer? Here you have it:

He cannot.

Turning Japanese

This morning colleague Sean Ring of The Rude Awakening half-quipped that the Bank of Japan’s director must have received blizzards of very sharp telephone calls from around Earth on Monday.

“Don’t you dare do that again!”

We hazard Mr. Ring is correct.

Thus Japan pays a steep, steep price for decades and decades of currency debasement, interest rate manipulation and kicking cans down roadways.

Yesterday’s difficult choice becomes today’s more difficult choice becomes tomorrow’s impossible choice.

Japan is in an impossible fix today because it refused to confront yesterday’s difficult choice.

Only by happy accident — boasting the world’s premier reserve currency — has the United States avoided an identical fix.

Yet as the world attempts to wriggle itself out of the dollar, that happy accident may switch to an unhappy accident in the years ahead.

On some semi-distant tomorrow… the United States may well and truly turn Japanese…

Comments: