Positioned For a Historic Crash

Earlier this week, Donald Trump’s victory in the 2024 presidential election was officially certified by lawmakers in a joint session of Congress.

Kamala Harris presided over the ceremony as president of the Senate and faced the awkward task as she formally certified Trump’s victory and her own loss.

Notably, the Democrats set aside some members’ views that Trump is ineligible to return to the presidency because of the Constitution’s bar on insurrectionist officeholders.

Apparently, the voice of the American people resonated in Democrat lawmaker’s ears because of Trump’s Electoral College landslide, his victory in all seven swing states, and the fact that he won a majority of the popular vote — the first Republican to do so in twenty years and only the second to do so in thirty-six years. That gives Trump both a mandate for change and the goodwill to try.

However, this decision to not challenge the certification does not mean all is well for America and the financial markets. Wall Street has challenging times ahead as shown by a shaky end to 2024. The traditional Santa Claus Rally did not materialize, which was a surprise for many investors.

Since the beginning of December, stocks of all sizes and styles have struggled, apart from shares of a few mega-cap companies that have increasingly dominated the market.

With the 2024 election in the rearview mirror and Donald Trump set to take office on January 20, a meltdown is still a threat to markets.

Here are three threats to markets as we head into 2025.

- Market Melt-Up. Markets are at or near all-time highs based on every available metric: P/E ratios, CAPE ratio, market cap/GDP ratio, concentration risk, etc. This is accompanied by indexing, investor complacency and analyst euphoria. When such conditions have existed in the past, they have always been followed by market crashes of 50% to 90% unfolding over several years. Examples include Dow Jones (1929), Nikkei (1989), NASDAQ (2000), and S&P 500 (2008).

We are now positioned for an historic crash. The specific cause does not matter – it could be war, natural disaster, a bank or hedge fund collapse or another unexpected event. What matters is the super-fragility of the market when the trigger is pulled. This is why Warren Buffett has over $300 billion in cash and why central banks are buying gold. Prepare now. Don’t be the last one to know.

- A U.S. recession is coming. There are ample signs that the economy is headed for a recession (or may already be in one) including higher unemployment, lower interest rates, flattening yield curves, negative swap spreads, collateral shortages in Eurodollar markets, reductions in China’s reserve positions (not a sign of “dumping” Treasuries but a sign of a dollar shortage and a need to provide liquidity to banks), declining oil prices (despite output reductions), and others.

The emerging recession will cause a stock market drawdown as earnings are revised downward, consumer confidence crumbles, consumer discretionary spending hits a wall and precautionary savings rise. The world will not bail-out the U.S. economy because China, Japan, Germany and the UK are all slowing economically at the same time or already in contraction.

This is problematic for stocks independent of any crash potential. A word on lower rates. Low rates are not “stimulus”. They are associated with recessions and depressions and not the sign of a thriving economy. The Fed is not leading the rate market. They are following the market down. Of course, a recession could trigger a market crash. But even if it does not, recessions are typically associated with 30% declines in stock valuations over a year or less.

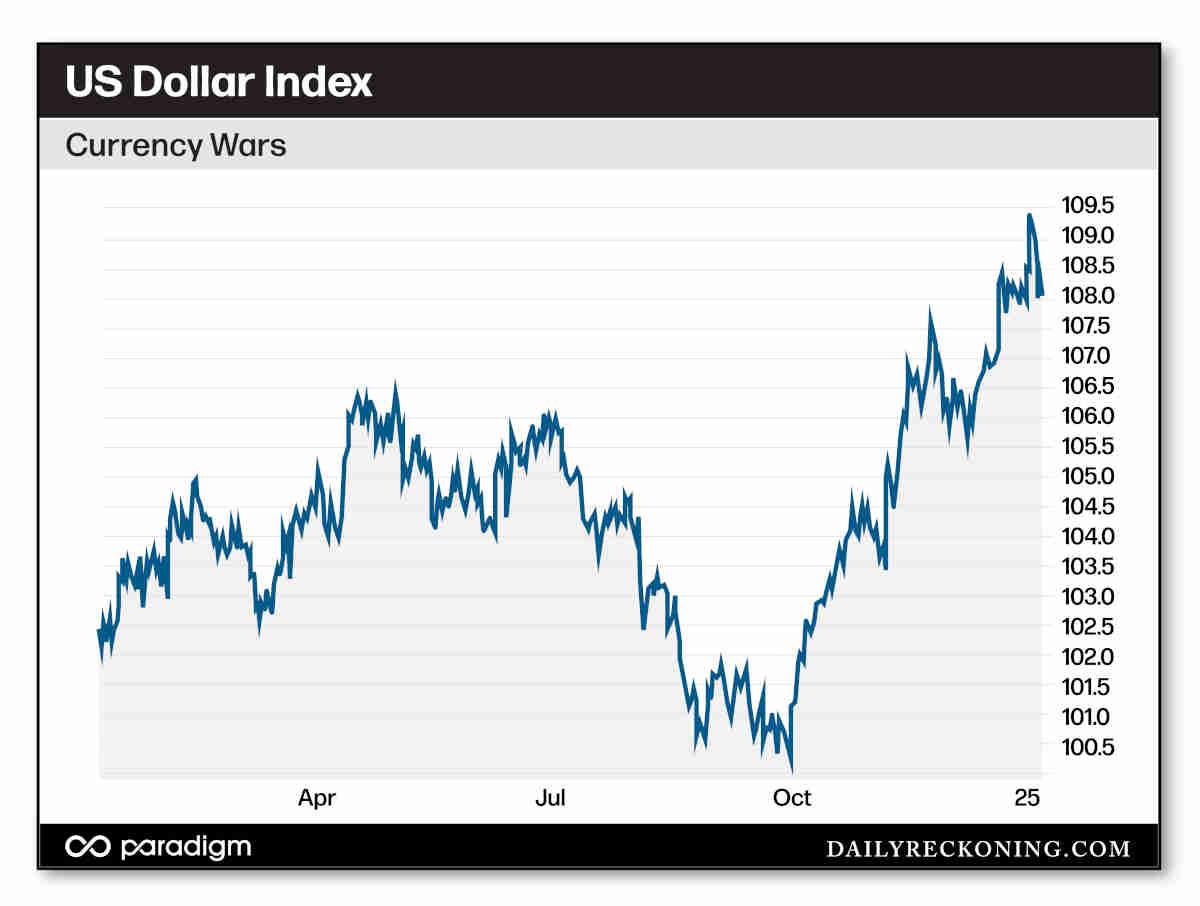

- Currency wars are back, and trade wars are coming. The super-strong dollar today makes it difficult for other countries to buy U.S. goods. Tariffs make the global dollar shortage worse as foreign investors seek dollars to jump the tariff walls and invest directly in the U.S. Both the strong dollar and the coming U.S. tariffs invite retaliation by trading partners who will put up their own tariff walls.

The result is a global contraction in trade that could resemble the trade collapse of the 1930s during the Great Depression. U.S. stocks fell 85% from October 1929 to June 1932 during that episode of trade wars. A repeat could be on the way.

Remember, the economy goes its own way. Business cycles have not been erased. The transition from Biden to Trump will bring economic pain as Trump inherits Joe Biden’s mess.

The U.S. economy (in contrast to economists) does not pay that much attention to elections or new administrations. It’s too big and moves to its own complex tempo. Investors may cheer the Trump policies and his reelection, but it will be a very bumpy ride in the first year of Trump 2.0.

Biden Isn’t Done Yet

Also, don’t underestimate what the Biden administration has been doing as they exit the White House. The fact is they can still do a lot of damage before Inauguration Day. What are they up to? Biden and company are trying to Trump-proof the presidency by signing contracts. Let me explain.

Remember the famous Inflation Reduction Act? Despite its name, the act actually increased inflation by being the Green New Scam in disguise. There was about $850 billion for garbage like windmills, solar modules, and green initiatives. A lot of the money went to the Democrat’s favorite contractors and electric vehicle makers. That passed in August of 2022, but guess what?

Most of the money hasn’t been spent yet.

So, now there is a mad scramble to sign contracts. You actually can’t spend the money that fast, but you can sign a contract with a five-year life or three-year life saying you’ll spend it over three years. And the idea is signing the contract now so that even when Trump becomes president, even though the money hasn’t been spent, it has been appropriated and it’s contractually bound.

And that’s the key. Bind the spending in contractual form so Trump can’t do anything about it.

These actions could cause havoc leading up to Trump taking office and beyond depending on how much damage they do. It won’t be a pretty picture for markets with so many companies impacted by these actions on top of a recession.

Bottom Line

After taking office, Trump’s agenda will incentivize billions of dollars of investments in U.S. energy and manufacturing jobs. He will make domestic oil drilling and refining a top priority which will provide America with energy independence. This will also benefit companies (and provide more jobs) in the energy sector.

But there will be plenty of minefields for markets to deal with in the first year as the transition takes place.

Comments: