‘Currency Wars’ Predictions Come True

Jim Rickards’ best-selling 2011 book, Currency Wars, was prophetic.

He painted a stark picture of the flaws in the modern paper monetary system, warning that “a new crisis of confidence in the dollar is on its way.”

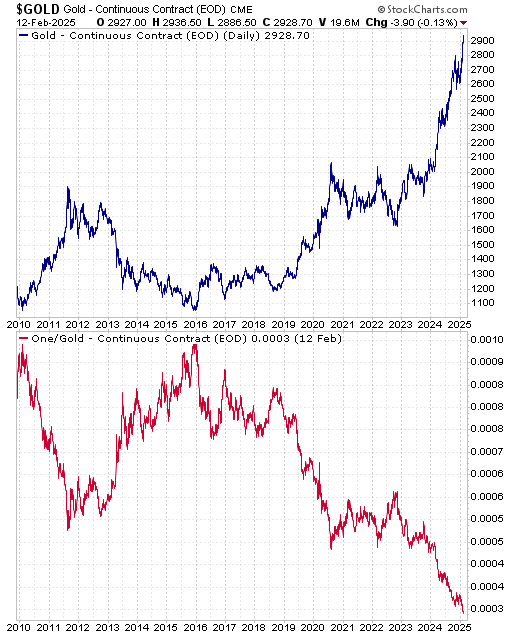

Although the U.S. dollar has been strong against most other paper currencies for years, it has weakened dramatically against gold.

Most people think of gold as a derivative of the U.S. dollar. That’s the blue line below.

Inverting the relationship is another way to think about gold. As shown in the red line, the dollar has lost 62% of its value against gold since 2015.

Reframing your perspective on the U.S. dollar as a derivative of gold, a timeless money, can be enlightening.

Let’s revisit currency wars 15 years after Jim popularized the term. Currency wars are no longer a theoretical discussion amid President Trump’s efforts to strike fairer trade deals.

The Pentagon’s Financial War Game: A Wake-Up Call

One of the best moments in Currency Wars comes from Jim’s firsthand account of a financial war game conducted by the Pentagon in 2009. In a secure war room at the Johns Hopkins Applied Physics Laboratory, experts from military, intelligence, and financial sectors gathered to simulate how nations might use currencies, sovereign wealth funds, and commodities – including gold – as weapons in economic warfare.

Unlike traditional war games, which focus on kinetic military conflict, this exercise centered on financial attacks. The U.S. team faced rival teams representing Russia, China, and rogue state actors. The objective? To see how a global currency war could unfold and whether the U.S. could defend itself in a financial conflict.

Jim recounts how his team introduced an unexpected move: Russia and China would coordinate to weaken the dollar by demanding gold-backed payments for energy exports. This was a radical departure from the conventional assumption that nations would act within the existing dollar-dominated system. The reaction from Pentagon officials was telling – the referees running the game deemed the move “illegal” and struck it from the record.

Steve Halliwell, a participant in the game, pushed back: “This is war! How can something be illegal?” This moment underscored a crucial reality – while the U.S. assumes the dollar will remain supreme, adversaries can devise alternate systems where gold, not paper money, dictates power.

The Pentagon’s ultimate takeaway was sobering. Even if the dollar collapsed in a future crisis, the U.S. still had one trump card: its vast gold reserves, which are stored on military bases like Fort Knox and West Point. This underscores gold’s enduring role not just as a store of value, but as a strategic asset of national security.

The Cyclical Return to Gold

Monetary history reveals a consistent pattern: when confidence in paper currencies wanes, gold steps back into the foreground.

Jim reminds us of a simple fact: “Gold has served as an international currency since at least the sixth century BC reign of King Croesus of Lydia, in what is modern-day Turkey.”

Nations have repeatedly turned to gold when paper money failed.

During the classical gold standard (1870–1914), currency stability and price predictability fueled global economic expansion. Jim cites a Federal Reserve Bank of St. Louis study that found economic performance under the gold standard was superior to the subsequent era of managed paper currencies.

In 1971, President Nixon closed the gold window, severing the dollar’s convertibility to gold. This event marked the beginning of the era of unanchored paper money, a period characterized by persistent inflation, rising debt levels, and recurring financial crises.

The Weaponization of Currency and the Shift to Gold

One of Jim’s core arguments is that modern currency wars – where nations deliberately devalue their currencies to gain trade advantages – have left the global financial system in a precarious position. He likens this to historical precedents, particularly the 1930s, when competitive devaluations deepened the Great Depression.

This dynamic is playing out today as countries seek to insulate themselves from Biden-era financial sanctions and currency manipulation.

Russia and China, for example, have aggressively increased their gold reserves. The shift is strategic: gold is not subject to counterparty risk or political interference, making it an ideal monetary asset in times of uncertainty.

This amusing cartoon from Merk Investments summarizes the currency wars as they apply to gold over the past 20 years.

We ignore or export gold, confident in eternal U.S. dollar supremacy, while China and other creditors trade dollars for gold.

As President Trump works to alter global trade deals, driving a harder bargain for the American worker, we’ll see plenty of currency volatility.

If economic rivals respond to tariffs by devaluing currencies (a classic currency war tactic), then investors around the world have yet another reason to own gold as insurance against monetary instability.

Gold and the Collapse of Confidence in Paper Money

The primary flaw of paper currencies, as Jim outlines, is their dependence on trust. In the absence of tangible backing, money relies entirely on confidence in governments and central banks.

However, history shows that this trust is fragile.

“The claim that the dollar is a store of value has collapsed due to a total lack of trust and confidence,” Jim warns.

The BRICS nations are exploring alternatives to the dollar, with discussions of a gold-backed trade settlement system gaining traction. Trump clearly does not like this trend, but it’s one of the costs of pursuing a long-overdue agenda of refocusing the U.S. economy on production. Buying more gold is a natural portfolio hedge for foreign trading partners and adversaries to make.

As the cracks in the paper system widen, gold offers a compelling solution. Unlike paper money, it cannot be printed at will. It is a finite resource with intrinsic value, making it an ideal anchor for a stable monetary system. Jim suggests that a future financial crisis could force a return to a gold standard, albeit at a much higher price…

Note from Adam: Members of Strategic Intelligence Pro can read the rest of this research, along with the accompanying options play, here.

Comments: