Biggest Recession Warning in 42 Years Just Tripped

Mr. Powell frightened the horses yesterday.

The Dow Jones Industrial Average plunged 532 panicked points on his congressional testimony that:

We continue to anticipate that ongoing increases in the target range for the federal funds rate will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time. In addition, we are continuing the process of significantly reducing the size of our balance sheet…

The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes. Restoring price stability will likely require that we maintain a restrictive stance of monetary policy for some time.

Our overarching focus is using our tools to bring inflation back down to our 2% goal and to keep longer-term inflation expectations well anchored. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run. The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

Echoes from yesterday’s testimony were dinning in the ears today — the Dow Jones retreated another 58 points.

Fade the Pivot

And so Wall Street’s cherished “pivot” fades further from view… toward the distant horizon.

Wall Street not only confronts a gentle 25-basis-point rate pinprick this month — but a mighty 50-basis-point clout.

The market presently gives 77.9% odds of a 50-basis-point rate increase at this month’s Federal Reserve confabulation.

Just one week prior those odds came in at 29.9%. And one month prior? A mere 9.2%.

The evidence is clear, the evidence is decisive. For Mr. Powell and mates… the way forward is the warpath.

They maintain a fantastic devotion — a nearly monomaniacal devotion — to scotching inflation.

Wall Street can just go scratching, they appear to say. Their reputations as central bankers take far greater precedence. “Price stability” takes far greater precedence.

Tightening Into Weakness

Yet as Jim Rickards has argued in these pages… often and fiercely… the Federal Reserve is “tightening into weakness.”

That is, the Federal Reserve is elevating interest rates and axing the balance sheet as the economy itself is losing oomph.

It is kinking the hoses at a time of already trickling flow. How much more can it squeeze without running things dry?

And today we are informed that the hose is in fact running dry. The economy is in for a good hard parch.

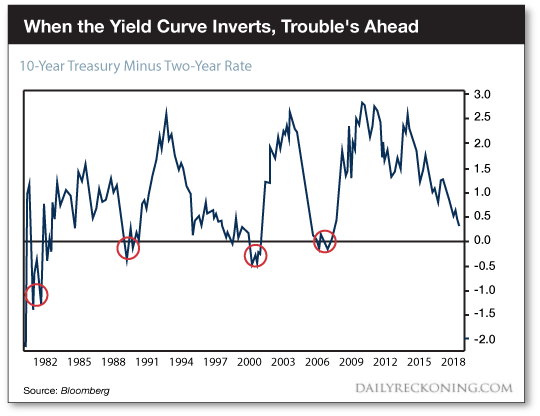

Yahoo Finance informs us that “the Treasury market is sending its sharpest warning about recession risks since 1981.”

The nation is 42 years removed from 1981 — quite a spell. Not once during that entire span has the recession klaxon wailed louder… if the report has truth in it.

A Bizarre Anomaly

The Treasury market’s shrieks center upon the “yield curve.” The yield curve?

The yield curve is simply the spread between short-term interest rates and long-term interest rates.

Long-term rates normally run higher than short-term rates. For the reasons, we needn’t look far.

Investors, for example, demand greater compensation to hold a 10-year Treasury than a 2-year Treasury.

They are, after all, locking away their money for 10 years — as opposed to two years. Wouldn’t you demand greater compensation under the 10-year option?

And the 10-year Treasury yield rises when markets anticipate higher growth… higher inflation… higher animal spirits.

But the further out in the future, the greater the uncertainty.

Thus the 10-year yield should therefore run substantially higher than the 2-year yield.

But when the 2-year yield and the 10-year yield begin to converge, the yield curve is said to flatten.

The First Signs of Trouble

And a flattening yield curve is a possible omen of lean days — and lean nights.

Is a flattening yield curve an immediate menace, a thundercloud overhead?

Not necessarily, say the experts. Not necessarily.

The yield curve can stay good and flat for a while — with no ill effects. Bloomberg’s Tim Duy:

The [yield] curve was extremely flat during the second half of the 1990s, a stretch of high growth. Only late in that period did the yield curve invert, finally foreshadowing the 2000 recession.

Only when the yield curve inverts do the klaxons begin their fusses.

Here is the graphic evidence, stretching to 1980 (we omit the 2020 recession due to its “unnatural” origins):

And as Yahoo Finance advises us:

On Tuesday, the difference in the yield on 2-year and 10-year Treasury notes further inverted, with the yield on the 10-year falling 103 basis points, or 1.03 percentage points, below the yield on the 2-year yield. This dynamic has preceded each of the last eight U.S. recessions.

Sound the Alarm!

1.03% is a handsome inversion. Glance again at the chart. Only the inversion preceding the hellacious 1981-82 recession excels it. Do you see?

The passage cited notes that “the difference in the yield on 2-year and 10-year Treasury notes further inverted.”

The backwardsness, the distortion, the inversion, actually entered effect last July.

The business got going under the Federal Reserve’s breathless rush to elevate interest rates beginning last March.

It is important to recall that the Federal Reserve lacks direct control over the 10-year yield and the 2-year yield.

It can only influence them. It cannot control them.

But being shorter term and closer to the Federal Reserve’s mass, the 2-year yield is greater influenced by the pushes and pulls of the Federal Reserve’s gravity.

And the Federal Reserve’s current rate hike cycle has worked tremendous upward pressure, gravitational pressure, upon this key rate.

Today the 2-year Treasury note yields an upward-pressured 5.07%. The 10-year Treasury note — further removed from the Federal Reserve’s gravitational influences — yields a curve-inverting 3.97%.

That, again, is the greatest spread in 42 years. Thus the Treasury market gives off the loudest recession alert in 42 years.

When — then — can you expect the recessionary hammer to come lowering?

Drumroll…

History reveals the catastrophic effects of an inverted yield curve only manifest an average 18 months post-onset.

Let us assume the present inversion proves no exception. The inversion predates the recession by 18 months.

We conclude the economy may peg along until… January 2024.

Recession comes in next January.

Of course we deal with averages. The blow may come landing later than next January. There is even the chance — however diminished in our estimation — that it may never connect at all.

Yet there likewise exists the possibility that the flattening blow could land much earlier and without warning.

Thus we part with this advice for the Hon. Jerome H. Powell:

Beware the sucker punch…

Comments: