Betrayed by the Dip!

If you’re reading this, you managed to survive last week’s brief but hair-raising stock market horror show.

No, the world didn’t end during the Yen carry trade panic. In fact, the S&P 500 finished the week lower by less than a tenth of a percent. Not bad! The 3% skid on Monday was the large-cap index’s worst one-day performance since 2022. To all but erase that kind of one-day move in less than a week is downright impressive.

Thanks to some eager dip buyers, this summer volatility spike hasn’t led to any serious pain. Despite the VIX ramping up to levels we hadn’t seen since the Covid crash, investors were far from fearful last Monday as they raced to pick up “cheap” shares of their favorite stocks.

Axois reports that Interactive Brokers data showed that “clients saw Monday’s selloff as a buying opportunity rather than a reason to get out of the market,” as buying picked up in popular names such as NVIDIA Corp. (NVDA), Tesla Inc. (TSLA), and Amazon.com Inc. (AMZN).

The mega-caps weren’t the only plays attracting the bulls. Leveraged tech ETFs like SOXL and TQQQ also experienced increased buying activity, Axios notes. Hey, if you’re going to BTFD, you might as well do it in style…

It doesn’t take any deep market knowledge to see why investors were so eager to grab shares last week. Like any powerful bull market, this year’s rally has rewarded dip buyers without fail. When it comes to the big, popular stocks, every single drawdown was a strong buying opportunity.

NVDA is the perfect example of just how powerful the buy-the-dip phenomenon has been this year. Here we have a highly visible market leader that has shoved the major averages to new highs. The stock fell double-digits during last Monday’s Yen carry meltdown, yet buyers immediately stepped in to scoop up shares.

Recession fears, the failure to post new highs last month, and an upcoming earnings report – none of these situations seem to faze investors who eagerly backed up the truck last Monday. They’re back at it again this week as NVDA offered refuge during yesterday’s choppy session, gaining 4% as the Nasdaq finished near breakeven.

I can’t tell you how it’s all going to play out. But I do know dip buyers will continue to push their chips in the middle until they’re eventually crushed.

Can they survive a deeper drawdown?

We might soon find out. While the initial shock of last week’s quick drop has dissipated, we’re now facing the possibility of much choppier conditions as the market attempts to regain its footing.

Is the Market Losing its Mojo?

I’m not predicting a big crash (or a spectacular rally, for that matter). But I do believe the market is potentially at its most vulnerable point since the melt-up rally began late last year. If there was a time when the dip might finally betray the early buyers, this could be it.

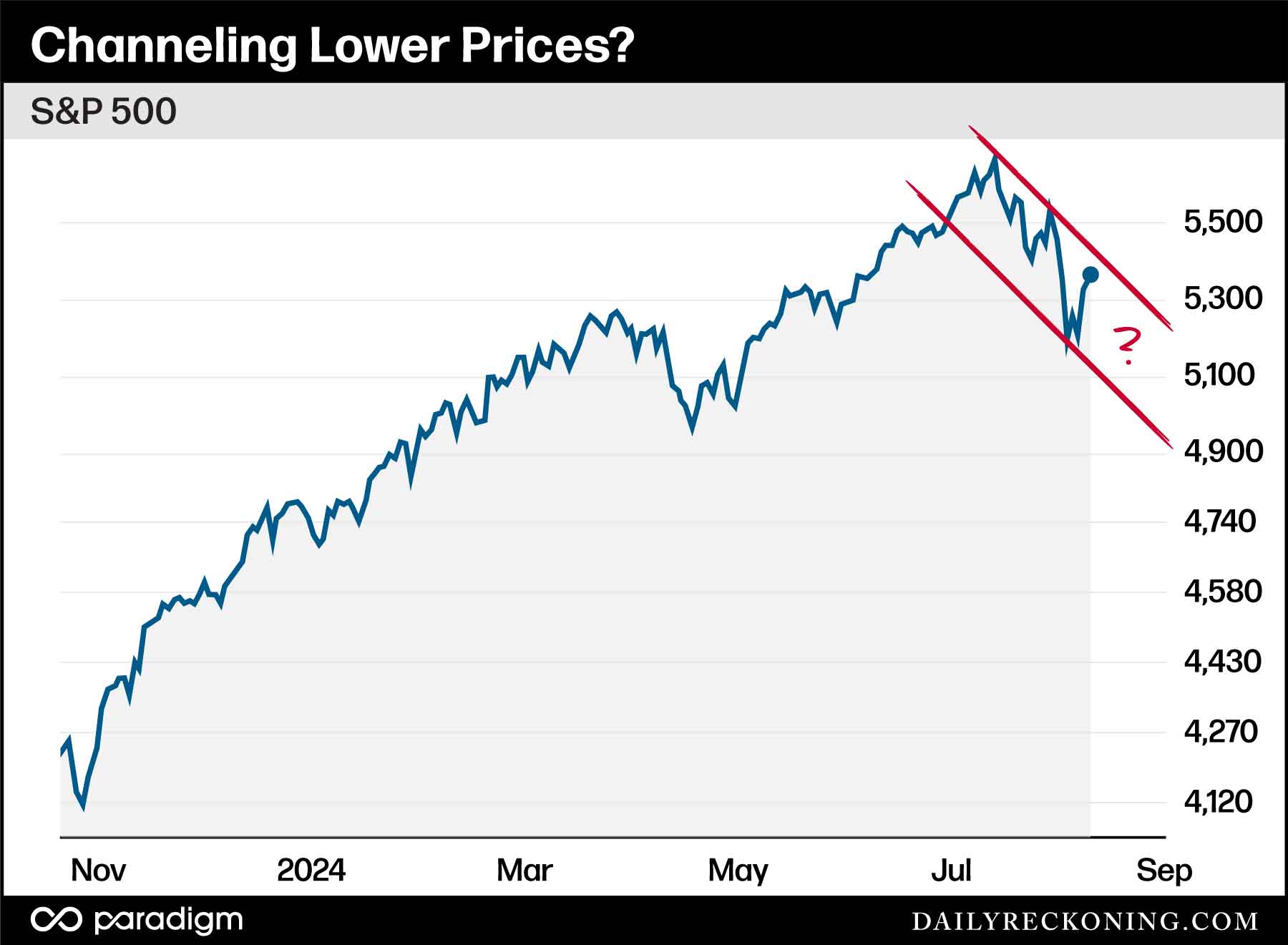

For starters, it’s important to note that the major averages had turned lower before last Monday’s Yen carry trade scare. The S&P 500 topped out nearly a month ago in mid-July and had posted three straight weeks of declines before volatility popped and everyone headed for the exits.

Could the S&P in the process of forming a corrective channel over the past four weeks? I think this is one possible conclusion. If it’s true, last Monday’s lows simply represent a logical spot for a short-term bounce – the bottom of the downtrending channel.

This would also mean the S&P would need to close the Aug. 2 gap and extend to approximately 5,450 in order to break the current short-term downtrend.

Is this move possible? Of course! And if a sharp rally does materialize here, plenty of buyers will gobble up shares and shove the markets back to all-time highs.

But if the S&P bumps its head at the top of this channel and fails to climb back above 5,400 in a timely fashion, a retest of those Monday panic lows are probably in our future. The 200-day moving average (not pictured in the above chart) near the April swing lows at 5,000 looks like a reasonable landing area. This also matches up well with the bottom of our downtrending channel.

To be clear, a drop to these levels would not kill the current bull market. We’re not talking about a crash or anything else out of the ordinary. Overall, this move would mark a peak-to-trough drawdown of approximately 11%. That’s normal behavior, especially considering the strength on display during the first half of the year.

Surviving Another Data Dump

The bulls’ work isn’t finished yet. Now, buyers will also have to navigate a barrage of economic data this week that could set the tone for the rest of the month.

First up: the market runs the inflation data gauntlet. PPI came in first this morning and was weaker than expected, earning a positive market reaction. CPI hits on Wednesday, followed by retail sales on Thursday. Obviously, CPI is the big number everyone is watching. Bloomberg reports that Citigroup options data indicated the S&P will move 1.2% in either direction on the CPI release.

Economically sensitive investors are looking for any clues that will offer a little clarity as to which way the Fed might move next month. A hot or cool CPI could begin to swing the odds of the expected September rate cut, which is currently a dead heat between a 25 basis-point cut vs. a 50 basis-point cut.

Is the so-called “soft landing” still in play? Or is the dreaded R-word (recession!) going to creep back into the picture?

These are the forces we’re dealing with in this crazy late-summer market.

Don’t be surprised to see the overall market remain choppy for the next few weeks, potentially sucking in overeager traders on some false moves. Bottom line: This is NOT the type of environment where we can just trade any stock that’s caught a bid and is moving higher on any given day.

We can also expect overreactions to the data and any other surprises the financial media might toss out this week. Remember, the news is always changing. But people are the same as they’ve ever been. The lizard brain always wins! It’s the most predictable aspect of any big investment question.

Comments: