Are The Ivies Well Endowed?

For decades, the Ivy League has been treated as a sort of financial Olympus—an elite club where money flows like vintage Bordeaux and the only financial hardship is deciding which fund manager gets to manage the latest billion-dollar donation.

Harvard, Yale, Princeton… the names alone conjure images of investment portfolios so dense they have their own gravitational pull

But here’s the inconvenient truth: those war chests aren’t nearly as invincible as they look. Underneath the towering prestige and carefully curated mythology, the Ivies have the same problem as every overconfident Wall Street whale: they’re asset-rich but liquidity-poor. That’s another way of saying: lots of numbers on paper, not nearly as much cash in the bank.

Paper Fortunes, Real Problems

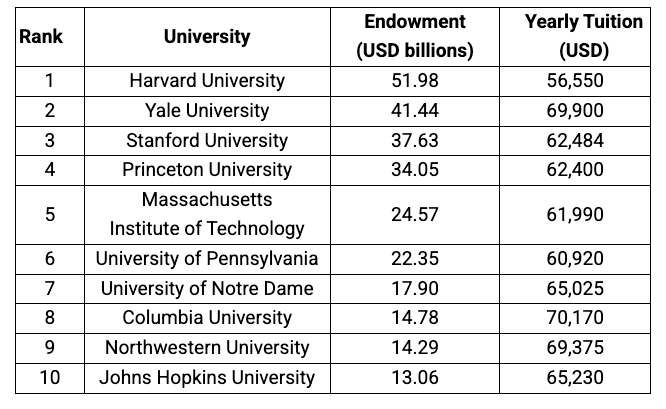

On the glossy brochures, the endowment totals are staggering. Harvard’s around $52 billion. Yale’s somewhere north of $40 billion. Princeton’s sitting pretty with $34 billion or so. Sounds like financial immortality, right?

Wrong. Much of that “wealth” is tied up in illiquid, high-risk bets—private equity deals, venture capital moonshots, commercial real estate in places that look good in an investor deck but take years (or decades) to exit without losing your shirt.

This is the so-called endowment model—beloved in the 1990s and early 2000s—where you stuff your portfolio full of alternative assets to chase returns the boring old stock-and-bond crowd can’t match. In a roaring market, it’s genius. In a downturn, it’s like trying to pay your mortgage with jelly beans.

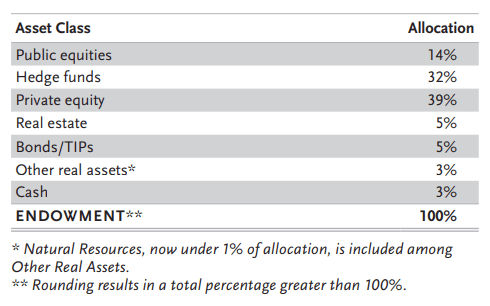

Note that Harvard’s endowment as of October 2024 only allocated 14% of its portfolio to public equities, 5% to bonds, and 3% to cash. The remaining 78% is allocated to alternative investments.

Credit: Harvard Management Company

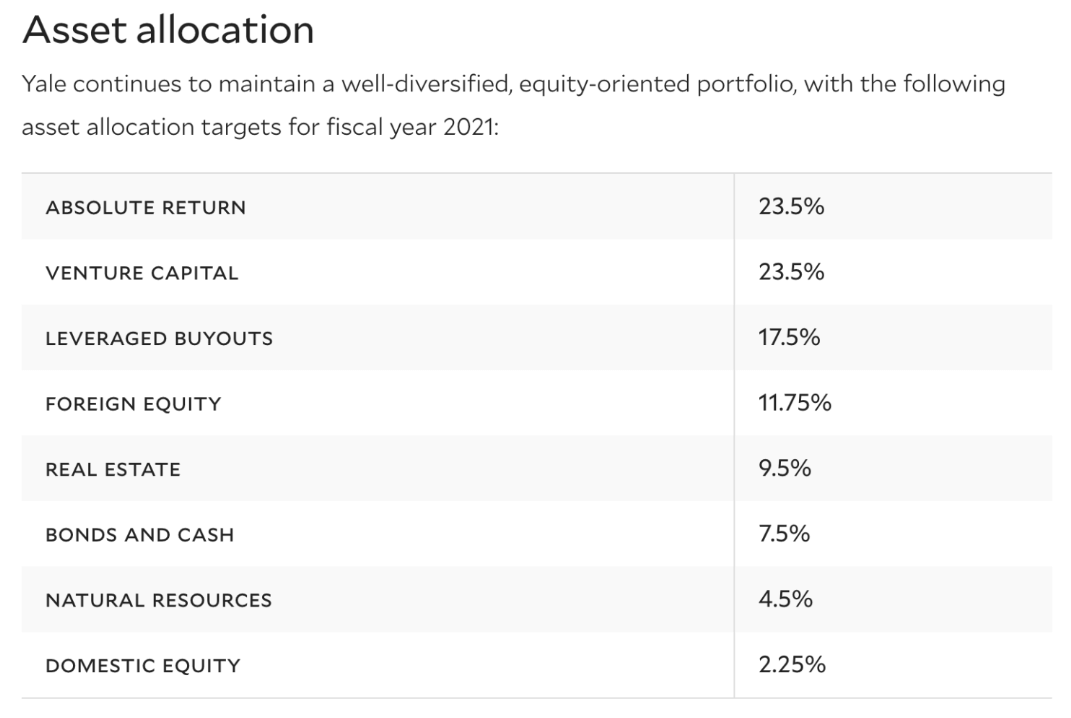

Yale stopped reporting their asset allocation. But the last time it did in 2021, only 2.25% of the fund was invested in domestic equity.

Credit: Financial Samurai

Try to remember that downturns happen. Big ones. These schools have already had to unload slices of their private equity portfolios—not because they spotted a killer deal elsewhere, but because they needed the cash now. You don’t dump illiquid assets in a slow market unless you have no choice. It’s the institutional version of pawning grandma’s silverware.

The PR Game: Look Rich, Act Broke

Here’s where it gets deliciously hypocritical. The Ivies love to tout their endowment size when they want prestige points—“Look at us, the wealthiest university in the world!”—but when anyone asks why tuition is $65,000 a year or why adjunct professors qualify for food stamps, suddenly they turn into Oliver Twist. “Please, sir, may we have some more?”

It’s a neat trick: look rich to donors, act broke to politicians, and use both narratives to your advantage. But that balancing act is getting harder. Because now, for the first time in decades, someone’s calling their bluff.

Politics Crashes the Cocktail Party

Perhaps Penn shouldn’t have tried so hard to disown The Donald, because the cozy days of quietly compounding tax-free billions are over. The political winds have shifted, and they’re blowing straight into the mahogany-lined boardrooms of the Ivy League.

Lawmakers—especially the ones who couldn’t care less about the alma maters of America’s elite—are aiming for those gilded balance sheets. New tax rules are already in motion, set to increase the levy on mega-endowments significantly. We’re not talking token gestures here—we’re talking taxes that could skim hundreds of millions off the top every single year.

Then there’s the regulatory sledgehammer: talk of stripping tax-exempt status, slashing federal research grants, and tying funding to political compliance. And unlike market cycles, which the Ivies can usually ride out, political cycles can get very personal, very fast.

When Illiquidity Meets the Tax Man

Now put it together: you’ve got a portfolio loaded with assets you can’t easily sell without taking a hit, and suddenly your annual tax bill spikes, your federal funding dries up, and the political climate turns hostile. That’s an existential threat.

Sure, you can still post a press release saying your endowment is “valued” at $40 billion. But if you can’t quickly turn that number into spendable cash without tanking asset values, it’s not much different from owning a priceless painting when your creditors are at the door.

The Real Victims? Not the Trustees

Of course, the trustees won’t suffer—they’ll still get chauffeured to board meetings and summer in Nantucket. No, the people who’ll feel the pinch are the ones who can’t afford to be in the room where the sausage is made:

- Students will see tuition hikes justified as “necessary to protect academic quality.”

- Faculty will face hiring freezes, smaller research budgets, and more red tape to secure funding. (Forgive me if I remain dry-eyed over this.)

- Staff will watch as “cost-saving measures” always seem to start with them. Yes, these overloaded administrative automatons need to be fired… yesterday.

Meanwhile, the schools will quietly shift their investment strategies to chase higher short-term returns—because nothing says “long-term academic mission” like throwing your portfolio into whatever asset class happens to be hot this quarter.

Hedge Funds With a Side Hustle

Let’s be blunt: Ivy League endowments are hedge funds with a university attached. The educational mission is the branding; the portfolio is the business. The problem is that the business is showing cracks, and the brand can’t cover them forever.

And when you think of them as hedge funds, their recent behavior makes perfect sense. Selling illiquid assets at a discount? That’s a liquidity crunch. Lobbying against new taxes? That’s protecting the carry. Cutting costs in the “non-revenue” divisions (a.k.a. departments that don’t land big corporate sponsorships)? That’s streamlining operations.

If Bridgewater ran a college, it would look a lot like Harvard.

The Prestige Trap

Here’s the final irony: prestige is the one asset they can’t sell, but it’s the one they’re most desperate to protect. Prestige is what gets the donations, justifies the tuition, and lets them shrug off criticism with the academic equivalent of “Do you know who I am?”

But prestige evaporates faster than a private equity valuation in a recession. All it takes is a couple of bad years—cutbacks, public squabbles, high-profile faculty departures—and suddenly the halo slips. And when that happens, donors get skittish, applications dip, and the whole carefully balanced financial machine starts to wobble.

Wrap Up

The myth of the endlessly wealthy Ivy League endowment has been a useful fiction—for the schools, their alumni, and the media that loves to fawn over their numbers. But the cracks are showing. Between illiquidity, tax pressure, political targeting, and the inherent risk of their investment strategies, these institutions are a lot closer to the financial edge than anyone wants to admit.

The next few years will be telling. If the markets stay cooperative and the political heat dies down, they’ll muddle through, maybe even come out stronger (especially if the Fed starts cutting as precipitously as Treasury Secretary Bessent suggests).

But if asset values slip, taxes bite harder, and Washington keeps sharpening its knives, we may witness something the Ivies haven’t experienced in a century: a genuine cash crunch.

And when that day comes, the hedge fund with a school attached might finally have to make a choice—double down on the portfolio and risk the mission, or sacrifice the portfolio to save the school. Either way, it won’t look anything like the glossy brochure.

Until then, remember: an endowment’s size is just a number. Liquidity is reality. And right now, the Ivies’ reality is a lot less comfortable than they’d like you to believe.

Will The Donald usher in The Dissolution of the Universities, as Henry VIII did The Dissolution of the Monasteries?

That is the question.

Comments: