Warsh Declares Fed Independence

As we anticipated in Tuesday’s FOMC meeting preview, the Fed left interest rates unchanged at the June 17 meeting. This leaves the Fed funds target rate at 3.5%–3.75%, where it’s been since Dec. 10, 2025.

We’ll explain the Fed’s latest policy decision, the signals Kevin Warsh sent in his first meeting as chair and why they may mark the beginning of a very different Fed.

UPDATE: “Not the stale Bernanke-Yellen-Powell Fed”

First, here’s the text of the relevant part of the Fed’s press release issued at 2:00 p.m. ET on Wednesday:

The Committee decided to maintain the target range for the federal funds rate at 3.5% to 3.75%, in support of the Federal Reserve’s dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

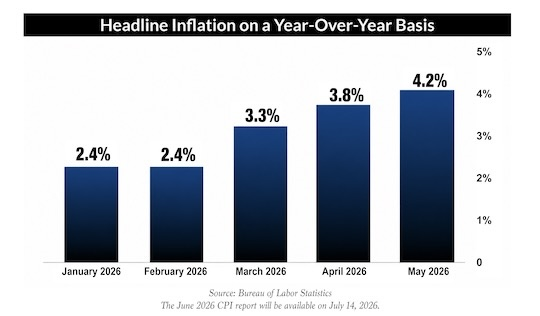

Inflation remains elevated relative to the Committee’s 2% goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

This meeting included a Summary of Economic Projections (SEP), which is a set of predictions on interest rates, unemployment, economic growth and other key metrics issued by the Fed governors and the 12 regional Federal Reserve Bank presidents.

These projections (known as the “dots” because they are presented as points on a graph) can safely be ignored. The dots offer some insight into current views, but they have little or no predictive value. They are almost always wrong.

The rationale for holding rates steady is straightforward. Inflation is not only above the Fed’s target of 2.0%, it has been rising rapidly and shows no immediate signs of coming down.

Meanwhile, unemployment has been steady between 4.3% and 4.5% since July 2025. That’s not particularly high and it has not been going up.

With inflation on the rise and unemployment steady, it was clear that the Fed would focus all of its policy initiatives on inflation.

As a practical matter, this meant that rates were definitely not going down. There was some sentiment for a rate increase, but this was outweighed by the view that inflation might come down on its own in the coming months as oil prices decline sharply due to the extension of the Iran war ceasefire and the prospect that the Strait of Hormuz will reopen soon.

This prospect was enough to avoid a rate increase for now.

Since this was Kevin Warsh’s first meeting as chair, there was certainly a view inside the FOMC that Warsh should begin his tenure with a strong show of support from committee members.

The result was a unanimous 12-0 vote to do nothing.

While the policy decision was a non-event, the meeting itself was highly significant.

New Chair Warsh used the FOMC statement and his press conference to make a number of important points. He made it clear that from now on this will be the Warsh Fed and not the stale Bernanke-Yellen-Powell Fed.

Here’s a summary of significant changes:

- Warsh personally declined to participate in the Summary of Economic Projections (SEP). This tells us two things: Warsh does not consider SEP important and he will probably get rid of the “dots” in the near future. Good riddance.

- The FOMC vote to approve the policy statement was unanimous. This is in contrast to recent meetings that incorporated dissents — including the April 2026 meeting — which had an almost unheard-of four dissents. That shows Warsh is firmly in charge for now.

- The FOMC statement was highly abbreviated, much shorter than statements have been for years. This reveals a Warsh policy that less is more. You can expect fewer leaks and wordy announcements from the Fed and more focus on listening to markets.

- The FOMC and Warsh himself did not offer any forward guidance. Since the rise of Ben Bernanke, the Fed has taken the view that by projecting inflation and growth expectations into the future, it could influence consumer and investor behavior in such a way as to achieve the targeted result. (This was always nonsense. I’ve met with Ben Bernanke, and he’s just as arrogant in person as he appears to be.)

Warsh knows that markets and the consumer economy are bigger than the Fed and they will go their own way based on more factors than the Fed can possibly influence or compute.

- Warsh created five independent task forces to review key functions of the Fed. These areas include communications, balance sheet management, the use of existing data, productivity and jobs in an era of transformation, and the Fed’s inflation framework.

The work of these task forces may take months or longer. But the topics themselves suggest material changes in how the Fed operates.

Likely outcomes are that the Fed will communicate less and listen more. It will likely reduce its balance sheet by selling, or not rolling over, intermediate- and long-term securities. The impact of AI on jobs will be an important focus. And Warsh is likely to favor more diverse inflation measures instead of the current preferred benchmark of core PCE.

Taken together, these developments do not just mark the beginning of a new chair. They mark the beginning of a new Fed.

The core of Warsh’s views and his new policies are contained in this excerpt from his press conference following the FOMC announcement:

We recognize that inflation has been running well ahead of the Fed’s long-stated inflation goal of 2%. That’s been going on for more than five years. Persistently high prices are a burden for the American people.

But the recent past need not be prologue. I am pleased to report that members of the FOMC are unambiguous and unanimous: This Committee will deliver price stability.

At any institution, a change in leadership is a natural and timely opportunity to reaffirm its mission, to review current practices and to consider whether those practices best meet our objectives.

On that score, you might have already noticed something: a difference in today’s policy statement. It’s a bit shorter, a bit simpler — and it dispenses with some older language.

That statement just gives you the facts, as best we can judge it. Absent, also, is so-called ‘forward guidance,’ which we agreed was not well-suited to the current policy conjuncture.

This afternoon you also received the usual Summary of Economic Projections. It’s been the practice of this Committee for participants to submit these projections, and I have encouraged my colleagues to continue to do so. I, however, have refrained from offering any projections of my own — consistent with my long-held views on the SEP, at least as currently structured.

In the median projections, real GDP rises at 2.2% this year, 2.3% next year, and total PCE inflation runs at 3.6% this year, 2.3% next year. The unemployment rate stands at about 4.3%. The median participant judges the appropriate federal funds rate to be at 3.8% at the end of this year and 3.6% at the end of next.

Reducing Warsh’s statements and initiatives to their essence, he is saying that the Fed will stop trying to lead markets and start listening to markets.

Markets are bigger than the Fed and they offer a wealth of information about the state of the economy — if you know where to look and how to interpret the data.

Yield curves, swap spreads, TIPS breakevens and other indicators are far more valuable than Fed junk science such as the Phillips Curve, forward guidance and wealth effects.

One can only hope that Warsh will be successful and the Fed will end its long history of being wrong about almost everything.

Institutional changes aside, the Fed’s dilemma over whether it should fight unemployment or inflation will be resolved. Inflation will come down on its own due to a slowing global economy and a likely recession. Unemployment will rise sharply for the same reasons.

The Fed’s interest-rate pause today will make both conditions worse, but its short-term obsession with inflation makes it blind to that outcome. Everyday Americans will pay the price as many lose their jobs and more businesses fail.

The next meeting of the Fed’s Federal Open Market Committee (FOMC) is scheduled for July 29, 2026. Given the uncertainties of the war in Iran and the impact of higher short-term and intermediate-term interest rates, the U.S. economy will be in a very different place by late July.

Comments: