Will the SpaceX IPO Zuck Early Buyers?

My friend and editor of Paradigm Press’s Million Mission, Davis Wilson, wrote a piece on the Facebook IPO I read with a potent mix of nostalgia and alarm.

I’ll start with the nostalgia.

The Big G

In 2012, I had already moved to Singapore, but was still flying back and forth to London, my old home, to meet and greet with friends and clients. One of my friends, G, was a partner at Goldman Sachs and had lived in New York since we graduated from London Business School together. But he had returned to London to work at Goldman’s Fleet Street offices. With a mathematics professor and an engineer for parents, G was a natural at the rather mundane mathematics finance employs. He made Goldman and himself bags of cash.

I loved hanging out with G because he was smart, fun, and rich as Croesus. But more than that, if I had to teach something that was over my head, he’d meet me in the pub to show me the ropes. One time, I had to teach a Credit Derivatives class. One glass of single malt scotch and two hours in the pub was all it took for me to have a Goldman-level understanding of the big picture. Definitions, pricing, uses, and back office requirements. He gave me it all, plus a few war stories, which the class devoured. The class certainly got its money’s worth.

Oh, those were fun times.

But the reason I bring G up is because of another conversation we once had about the Facebook IPO. I’ll never forget it for as long as I live, simply because I remember feeling my brain take in the information. It was the “scales falling from the eyes” moment for me, the moment I finally understood how cutthroat the business world could be.

Before META, There Was FB

META is pretty old news now, and its Metaverse is such a failure that they’ve stopped using the term. Reality Labs, Meta’s virtual reality (VR) division, has lost $83.6 billion over the last six years.

But back in 2012, Facebook was all the rage. It’s hilarious to think its biggest problem back then was that they hadn’t yet figured out online advertising. Of course, with the Facebook Pixel, they had mastered that domain and made themselves and their investors so much money they could piss it up a wall on a botched bet on VR costing billions.

Nevertheless, their IPO was hotly anticipated for many reasons, not the least of which was finally determining the company’s worth. Older readers may remember Diane Sawyer famously trying to weasel it out of Zuckerberg in an incredibly awkward interview. Think Mrs. Robinson meets Sheldon Cooper. Ewwww…

Morgan Stanley emerged as the lead bank after doing a lot of work for Facebook at no cost in the years leading up to the IPO. JP Morgan was second, leaving Goldman Sachs embarrassed as the third bank. (Even Facebook executives, with their close government connections, had no love for the “vampire squid.”)

But, as usual, this was an enormous blessing in disguise for Goldman. Morgan Stanley would screw up the IPO so badly that it took the massive reputational hit Goldman was able to avoid. How did Morgan Stanley mess up?

The IPO Numbers

On the surface, Facebook’s IPO looked like a triumph of capitalism. The book was 5x oversubscribed, so Morgan Stanley did exactly what it was paid to do: it raised the price from $28–35 to $34–38, jacked the share count 25% to 421 million, and handed Zuckerberg a tidy $100 billion valuation.

Facebook CFO David Ebersman had been quietly gunning for that number all along. Round, iconic, and utterly meaningless as a forward-looking metric, but perfect for a Wall Street dog-and-pony show.

But here’s the rot underneath the paint job: 11 days before the IPO, Facebook quietly whispered to Morgan Stanley that it was slashing its revenue projections. Mobile was eating desktop faster than Zuck’s ad team could monetize it; fewer eyeballs on ads, fewer dollars in the door. That’s a material development.

While Morgan Stanley’s institutional clients got that little heads-up, retail investors lining up to buy the hottest IPO in a decade were left staring at a glossy prospectus built on a lie of omission. The oversubscription number that made the deal look bulletproof? Engineered on asymmetric information.

And this is where the job gets sticky for bankers. On the one hand, you’ve got your issuing client; in this case, that’s Facebook. You want to maximize their take from the IPO. But on the other hand, you’ve got your investing clients, the pension funds, insurance companies, endowment funds, hedge funds, and other long-only asset managers who depend on the 10% first day bounce from the IPO price.

Morgan Stanley had just booked themselves 18 months of ass-kissing and discounts for the IPO buyers.

Was FB’s IPO a Failure?

The honest answer is, “It depends.”

For the IPO buyers? Yes. They got hosed.

For Morgan Stanley? Yes. The equity origination team utterly embarrassed the bank.

For Mark Zuckerberg? Absolutely not. It was the greatest day of his young life.

This brings me back to my conversation with G. I vividly remember saying something to the effect of “Ha! Morgan Stanley! What a failure…”

To which he replied, “Failure? For whom?”

I looked at him quizzically. I was confused.

“Seanie, Facebook raised $16 billion. Zuck never has to go to the market again!”

If you’re a well-worn mining investor, think of how many times you’ve been diluted in the past year alone.

Now, understand that Mark Zuckerberg has never done that to his shareholders. In fact, Zuck has had only one other equity offering, in December 2013, because Zuck had a tax bill due. Here are the stats on that one:

- 27 million shares sold by Facebook itself (~$1.5B, for working capital and general corporate purposes)

- 35 million shares sold by Mark Zuckerberg personally (proceeds used to cover taxes on exercising 60 million Class B stock options)

- 6 million shares sold by Marc Andreessen

That’s it.

So from Facebook’s perspective, it was maybe the greatest IPO of all time.

But for those Day One buyers… Ouch!

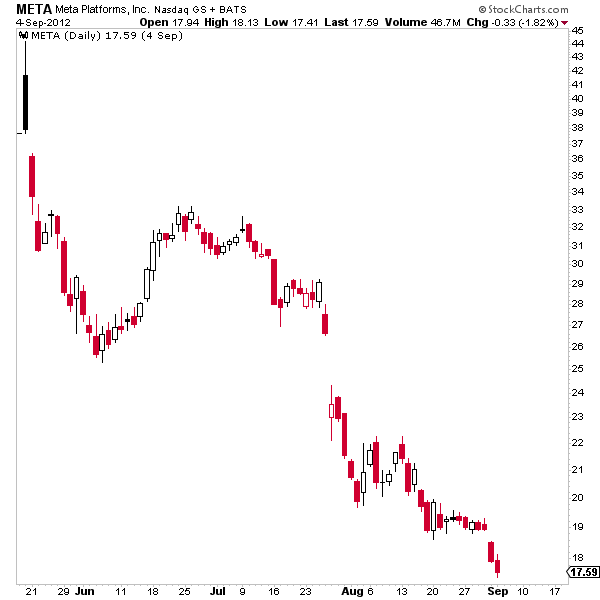

Let’s look at the chart.

After debuting at $38 and briefly hitting near $45 on the first day of trading, FB was cut in half over the next 5 months, closing at $17.59. If you’re a fund sitting on those losses, you’re bitching out your idiot banker every single day.

Allegedly, it took those 3 banks 85 subsequent IPOs over 18 months to make their institutional clients whole on the expected “money on the table” they’d been denied. Some hedge funds reported that shorting FB stock was their biggest profit that year.

Of course, Facebook became a darling for investors and has made people multimillionaires since.

Elon’s SpaceX IPO

Ok, here’s the alarm, after the nostalgia.

Please understand something. I’m writing this to you via my Starlink satellite dish because Telecom Italia can’t get its act together. I think Elon is a genius and an unambiguous good for the world, and I would’ve let him finish the DOGE job by gutting government spending.

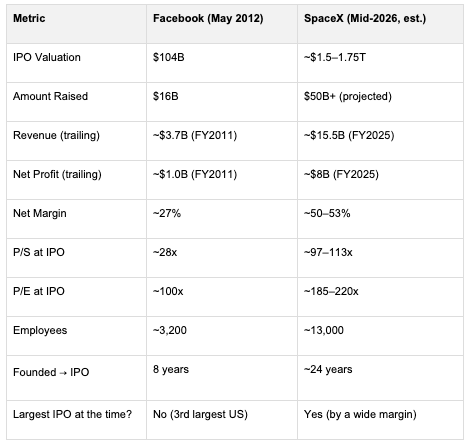

Here’s the comparison of FB’s IPO with SpaceX’s:

Elon is looking to raise $50 billion, and honestly, I hope he gets it.

But should you buy this stock?

Yes, but only after its IPO, when it falls at least 50% from these asinine, nosebleed levels the stock will get priced at.

I remind you of Scott McNealy’s reflection, years after Sun Microsystems’ stock imploded:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

At a P/S of circa 100, Elon has to give you 100% of revenues for 100 straight years as dividends… with all those other assumptions McNealy was nice enough to elucidate.

Good luck with that.

To reiterate, I think Elon is doing yeoman’s work for humanity. But I’m going to let bloated fund managers who benefited from decades of receiving Federal Reserve-induced funny money pay for it.

You should, too.

Wrap Up

Rarely has history screamed so loudly to warn us. Facebook’s IPO is our guide. SpaceX is in front of us.

While we cheer for Elon to reach for the stars… or just Mars… we mere mortals on Earth should tend to our flocks, rather than let this IPO clean our clocks.

Comments: