Loans to Nonbanks Threaten Banking Crisis

Last week, the Federal Deposit Insurance Corp released the industry data for US banks for 2025. On the surface, the numbers look reassuring, even strong. But beneath the calm headline figures lies a growing risk that investors should not ignore. Domestic deposits increased for the sixth consecutive quarter in Q4 2025 by $318.3 billion or 1.8%, the FDIC reports. Loans grew by 2% in Q4 and almost 6% YOY. Foreign deposits grew 11%, but subordinated debt and FHLB advances each fell ~ 14% as banks shed excess capital and funding.

U.S. bank loan growth in 2025 was robust, with total loans and leases reaching $13.4 trillion by year-end, a sequential increase in Q4 and a 5.9% annual growth rate, driven by larger institutions. Personal loan balances hit $2.2 trillion, while credit card debt rose 5.5% annually but the utilization rate for credit cards is still less than 20% of the total credit available. Yet behind this placid picture is a growing threat to banks and financial markets. At first glance, this looks like a healthy banking system. But that placid picture masks a fast-growing vulnerability that could become the next major pressure point for banks and financial markets.

The fastest growing bank asset category is loans to non-depository financial institutions (NDFIs), a corner of the financial system that regulators have struggled to monitor and control, up 7% in Q4 vs Q3 and up 35% YOY to $1.4 trillion at year-end 2025. With growing signs of credit stress among nonbank companies, banks will eventually pull back from lending to NDFIs. The problem is timing. By the time banks tighten lending standards, many private companies dependent on this funding may already be heading toward collapse, and those failures will not stay confined to the shadow banking system.

They will hit bank balance sheets directly.

The latest default involving UK mortgage issuer Market Financial Solutions threatens a £930 million shortfall in collateral backing loans to Apollo, TPG, other Wall Street private credit sponsors that are heavily involved with lending to private credit and equity, and various speculative ventures involving the current “AI investment boom.”

“The collapse of MFS, which attracted backing from firms including Barclays Plc, Apollo Global Management Inc.’s Atlas SP Partners unit, Jefferies Financial Group and TPG, is the latest crisis to hit both banks and direct lenders, and puts a spotlight on asset-based financing,” Bloomberg reveals. “Accusations of double pledging also emerged in the collapses last year of US auto parts supplier First Brands Group and sub-prime auto lender Tricolor Holdings.”

Accusations of double pledging collateral have also surfaced in recent failures such as First Brands Group and Tricolor Holdings, further highlighting the fragility of the system.

The fact that Apollo’s Atlas SP unit was caught unawares by the apparent collateral fraud at MFS is especially notable given the firm’s past experience. One of the leading providers of secured financing to nonbank mortgage companies in the US, Atlas SP was formerly owned by Credit Suisse and has been the advisor on numerous financing transactions for NBFIs. Yet two supposedly “secured” warehouse facilities backed by Atlas SP are now reported to be in default. If the lenders structuring these deals are surprised by collateral problems, investors should be asking deeper questions about how widespread these risks really are.

The collapse of American Car Centers in 2023, another Atlas SP client, provided advanced warning of a wave of corporate insolvencies that now threaten the US banking sector with contagion. U.S. corporate bankruptcies in 2025 surged to their highest level in 15 years, with over 700 companies filing for protection through November, marking a 14% increase over 2024. A large share of those failures involved private equity-backed firms.

Why is the rapid growth in bank lending to NDFIs a problem? Federal Reserve Chair Jerome Powell previously expressed that while non-depository financial institutions play a productive role in the economy, their growth outside the traditional regulatory perimeter poses risks to financial stability. We’re not talking here about mortgage companies with fully secured loans, but instead speculative credit and private equity schemes that are running out of cash.

The growth of private equity and credit is particularly problematic for banks. Many institutions are quietly masking early defaults through loan forbearance. When busted private equity firms cannot pay their debts, many seek to buy time by paying “in kind” with additional equity effectively issuing more of what the market already considers worthless. Paying “principal on original principal” or “POOP” (h/t Victor Hong) is one the thin canards used by private equity sponsors to conceal their financial malfeasance. In short: investors are being paid with more of the same failing capital structure.

In 2024, Federal Reserve Chair Jerome Powell expressed concerns regarding the rapid growth of non-bank financial institutions and the shifting of financial intermediation outside the regulated banking perimeter. He emphasized the need for regulators to be “smart” about where risks are emerging in this sector, noting that non-bank lending could lead to an overall lack of economic stability. But federal bank regulators have done little to address the explosion of lending to NDFIs. History shows that when a bank asset class grows significantly faster than the broader economy, it is usually a signal that systemic risk is building.

When you see a bank asset class growing far more quickly than the broad economy, this is a red flag that suggests potential systemic risk. But even more troubling that the high rate of growth in bank lending to NDFIs is the huge amount of undrawn loans available to these lightly capitalized companies involved in private equity and credit.

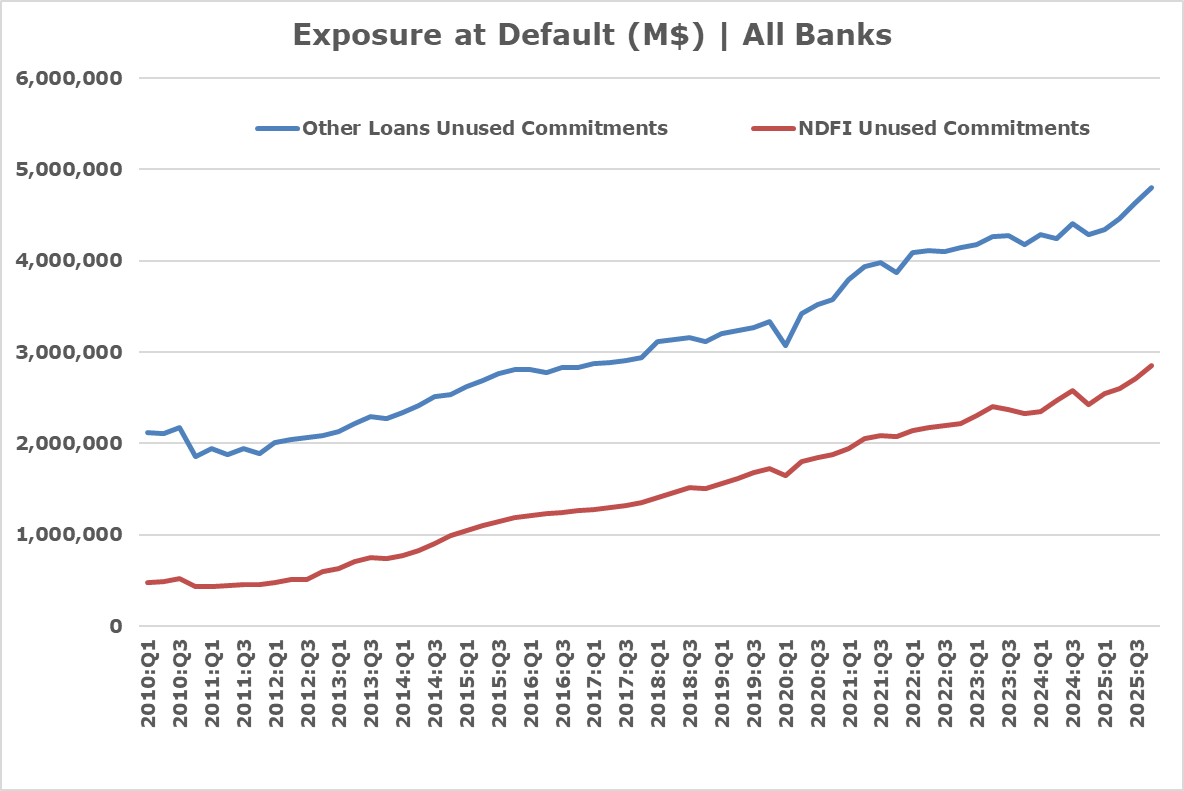

The FDIC does not yet disclose full loan category data on NDFI series, but we can infer from Other Loans line that banks currently have an estimated $2.8 trillion in unused loan commitments to NDFIs or exposure at default of 200% of current advances as defined by Basel III. A non-bank firm can draw on these contracted credit lines and immediately default, causing a massive loss to the bank lender. For every dollar of the $1.4 trillion in bank loans outstanding today to NDFIs, there are two dollars in undrawn loans or a total of $2.8 trillion, as shown in the chart below.

In practical terms:

- Banks have $1.4 trillion in outstanding loans to NDFIs

- They have another $2.8 trillion in undrawn commitments

That means for every dollar already lent, two more dollars are waiting to be drawn.

And a nonbank borrower can draw on those lines and default immediately, leaving banks with the loss.

Total potential exposure: roughly $4.2 trillion.

If stress spreads across private credit markets, that number becomes very important, very quickly.

Source: FDIC

The massive amount of bank lending to NDFIs is an approaching storm that has been largely ignored by federal regulators but is gaining growing attention from credit analysts. One public benchmark for the growing credit stress facing nonbanks is business development companies, which have seen an 18% decline in stock valuations over the past year vs an equal positive gain for the S&P 500. That divergence is not random. BDC investors are effectively voting with their capital that private credit risk is rising and rising quickly.

“UBS strategists say private credit could see default rates surge as high as 15% if artificial intelligence triggers an “aggressive” disruption among corporate borrowers,” the Swiss bank reports. “Direct lenders that financed software companies are exposed to AI’s impact, with some estimates suggesting 40% of all sponsor-backed loans are tied up in the software industry.” A 15% default rate is 2x the highest level of bank loan delinquency seen in 2008.

Put that number in perspective. A 15% default rate would be roughly twice the highest level of bank loan delinquencies seen during the 2008 financial crisis.

If even a portion of that scenario materializes, private credit markets, and the banks financing them, will feel the impact immediately.

The year 2025 was an extraordinary period for many reasons, including low credit loss rates and soaring asset values. QE teaches us that high asset prices suppress the cost of default, until asset values fall. But Wall Street is still trying to spin the growing delinquency among private companies as being only a problem “on the margins.”

“A review of the 3,649 middle market (MM) corporate credit assessments completed in 2025 shows mixed signals,” notes Kroll Bond Rating Agency. “Slowing growth is negatively impacting some companies’ credit quality, but overall, our portfolio remains stable. The growing divergence in performance is driven by challenged subsectors that we believe will contribute to the rising, yet contained, default rate in 2026.” In other words: the cracks are visible, but the market is still hoping the damage remains contained.

In the 1920s, many observers believed that asset values had reached a “permanently high plateau,” That confidence did not age well. This despite warnings from some observers of an impending collapse. Sectors like private equity and credit, and AI, all promise higher credit costs ahead. But for lenders, the immediate implication may be something very different: higher credit costs. When credit costs rise, earnings decline and stocks follow. The sharp declines in bank stocks in January and February illustrate this tendency.

We expect bank stocks to underperform their strong 2025 performance and face several challenges in the coming year:

- Rising credit costs

- Elevated market volatility

- Higher operating expenses

Banks will benefit from falling funding costs, which should provide some support for margins.

But the outsized credit exposure to nonbank financial institutions may become one of the dominant financial narratives of 2026.

If stress spreads through private credit markets, investors may quickly discover that the shadow banking system is not nearly as “separate” from the traditional banking sector as many assume.

Editor’s Note: Investors who want deeper analysis of bank balance sheets and emerging credit risks can follow Christopher Whalen’s ongoing research and commentary.

- Watch Chris on The Wrap with Julia La Roche, where he regularly discusses developments in banking, credit markets, and financial regulation. Also available on Apple Podcasts.

- Read more private market risk analysis here.

- Track performance using Whalen Global Advisors’ Top Bank Index, a proprietary benchmark covering leading U.S. financial institutions.

Access to the index and detailed bank research is available via Institutional Risk Analyst.

For investors navigating the evolving risks in the banking sector, independent analysis has rarely been more valuable.

Comments: