Exposed: America’s “Actual” GDP

Yesterday we explored the two dimensions of government spending — the seen and the unseen.

Today we throw additional light upon the unseen… and report a shocking discovery.

Has the entire post-recession “recovery” been a depression obscured by the false prosperity of debt?

The possible answer shortly…

As reported yesterday, The Wall Street Journal credits nearly half the GDP growth rate since last April to government spending — defense spending in particular.

We countered that the latest GDP numbers are phantom, that they conceal more than they reveal… as a well-executed toupee conceals a bald head.

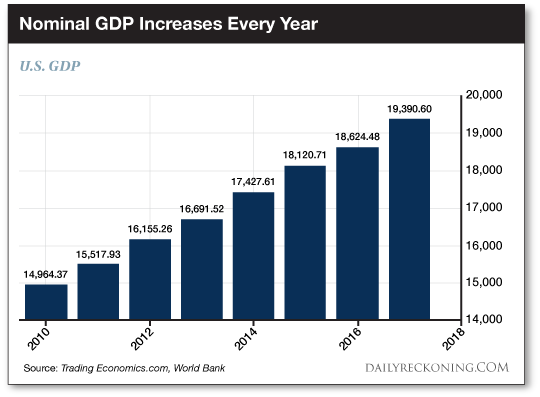

Between 2010–2017, nominal U.S. GDP expanded an average 2.2% per year — or thereabouts.

Some years it expanded more than others. But each year, nominal GDP expanded.

Meantime, the national debt has doubled since 2010. It now rises above $21 trillion.

And the Federal Reserve nearly quadrupled its balance sheet to nearly $4.5 trillion before its recent assaults upon it.

But how much of the post-recession growth is real… and how much is a debt-spun mirage, a shadow, a phantom?

What would GDP look like absent the artificial stimulus?

Last year financial advisory firm Baker & Co. Inc. hatched a study to answer these questions.

Their findings were… illuminating…

The government has borrowed luxuriantly for decades.

“Actual” GDP (details to follow) has always risen with the rising debt — whether because of it — or in spite of it.

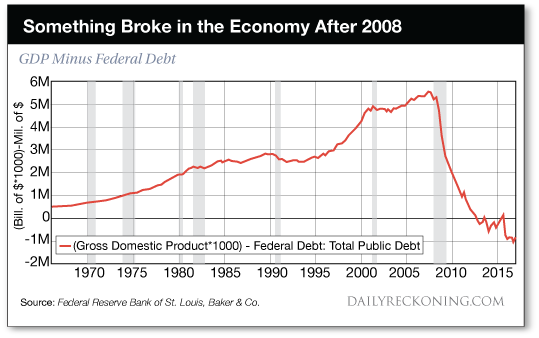

But after 2008, Baker & Co. argues, “Something in our economy broke.”

“Actual” GDP no longer rose with the rising debt.

In fact, they claim it has been falling.

They argue the phony fireworks of debt have thrown a smoke screen over the depression:

Since then, it appears the economy has been in what would be considered a depression but masked by huge federal government stimulus borrowing.

Their conclusion swims outside the mainstream… flouts official wisdom… strips the emperor of his garments.

But is it true?

At the heart of Baker’s tort is a trick the federal government uses to measure GDP.

It begins with this question:

If you take on debt, do you consider it income? Or do you take it at face — debt that must be repaid?

If you answered debt is income, we suggest you apply for a position within the Bureau of Economic Analysis.

In its calculations of GDP, government spending adds authentic bounce to the economy.

It makes no distinction between money the government raises through taxes… and the money it raises by borrowing.

Baker counters that the money government borrows must eventually be repaid.

Thus, it is not income. It is “artificial stimulus”:

[We] suggest that government debt is not part of “national income” because it is not income. It is borrowed… and must be paid back eventually… Debt is artificial stimulus, not national income! Governments must pay back debt either through higher taxes, inflation/depreciated currency, reduced services or some combination thereof.

Baker therefore created what they consider a measure of true GDP — the “Actual National Income.”

How does “actual” GDP appear without the smoke screen of debt?

Their shocking answer:

Examine the graph, says Baker, and “tell me if you think the actual economy has healed.”

We have. We cannot.

In fairness, the data do not cover 2018. But the point stands nonetheless.

How much oomph has the post-2008 barrage of debt given GDP?:

Since 2008, this artificial stimulus has averaged 7.45% of GDP. The arithmetic… is quite simple; without the artificial stimulus created by spending the proceeds of newly issued Treasury bonds, our GDP has declined an average of 7.45% each year since 2007!

Kind heaven, can it be — has actual GDP declined an average 7.45% each year since 2007?

And if that artificial stimulus is removed?:

With the federal government borrowing and spending over 6–7% of GDP, then it stands to reason that without the government’s ability to borrow new money, GDP would collapse 6–7%.

For emphasis:

Remove the stimulus and GDP collapses up to 7% — if the theory hangs together.

Prominent economists Carmen Reinhart and Kenneth Rogoff have shown that annual economic growth falls 2% per year when the debt-to-GDP reaches 60%.

When it hits 90%, growth is “roughly cut in half.”

When did the U.S. debt-to-GDP ratio nick 90%?

In 2010 — shortly after “something broke” in the economy.

What is America’s current debt-to-GDP ratio?

Roughly 105%.

Meantime, the Congressional Budget Office (CBO) projects deficits will approach $1 trillion next year.

It further forecasts deficits will exceed $1 trillion in 2020, where they may remain for the next decade.

We can only conclude that something is still broken in the economy… and will stay broken until proven differently.

Regards,

Brian Maher

for The Daily Reckoning

Comments: