Dieselflation Sparks Energy Emergencies

I hope you had a good Easter weekend. It’s back to business now, and oil and refined fuel prices are up-up-up. There’s much to discuss because we want to stay ahead of the game.

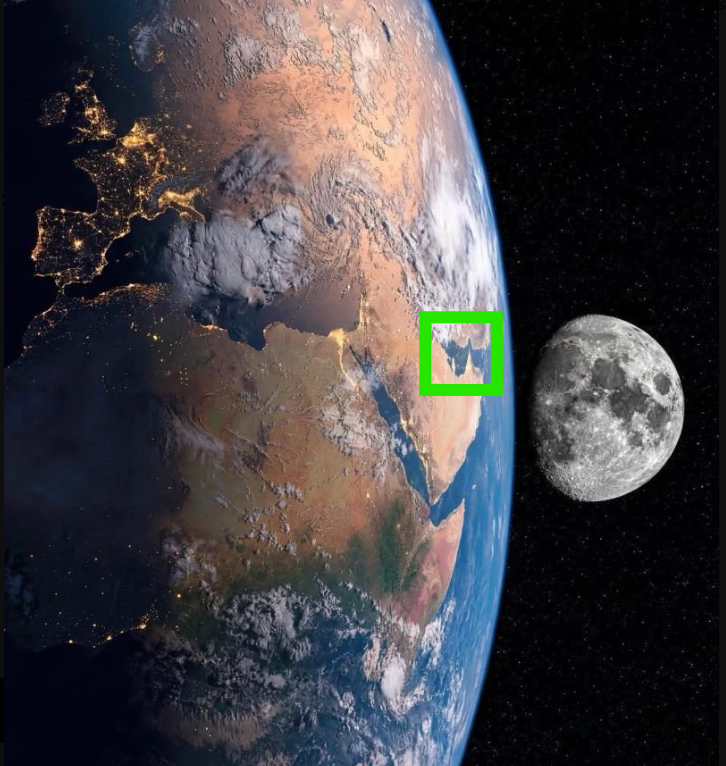

First, though, it’s worth noting that out of eight billion people on our world, a mere four (4) spent the past few days headed to the Moon. Nice work, if you can get it.

North Africa, Europe, Eurasia and Persian Gulf (green box), plus Moon. Courtesy NASA.

I mention the Moonshot because, as you can see, we have an awesome photo of Earth and Moon together. To me at least, this image helps frame some of the issues.

Moonshots While the World Keeps Spinning

In the center of that photo above is the brown Sahara of North Africa, with the Red Sea and Arabian Plate just to the east. To the north is the Mediterranean Sea, and then Europe framed by lights that shine against a dark background. And of course, Eurasia is further east and northeast. Plus, there’s that (editorially added) green box around the Persian Gulf; aka “Arabian Gulf,” depending on who you talk to.

In the big view of things – looking down from 250,000 miles away – while we all went about our life on earth this past weekend, and even for the four souls out in space, the world kept spinning.

Certainly, the Iran war continued, complete with white-knuckle excitement over the rescue of American personnel from behind the lines (another discussion for another time). While closer to home I noticed that the price of diesel fuel rose by about 60-cents at the end of last week.

Both of these things – Iran and diesel – are connected, and that’s today’s theme. In other words, the war has driven up oil prices, which means that diesel and refined fuels are getting expensive, and absolutely it means we’ll have inflation ahead. “Dieselflation,” so to speak.

So, let’s dig into what’s going on…

Well-Traveled Barrels of Oil

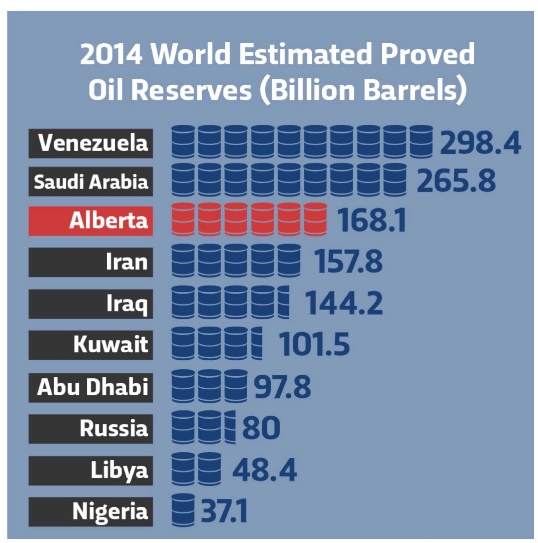

There’s a lot of oil in the world; it’s all over the place. But much of that oil is in the Middle East, as you can see from this graph that ranks various nations and their estimated oil reserves (in billions of barrels).

Estimated oil reserves by nation (and Alberta). Courtesy @RazorOil.

Obviously, we see familiar Middle East names here: Saudi Arabia, Iran, Iraq, Kuwait and Abu Dhabi. All export oil, and the graph doesn’t include Qatar which is a major natural gas player.

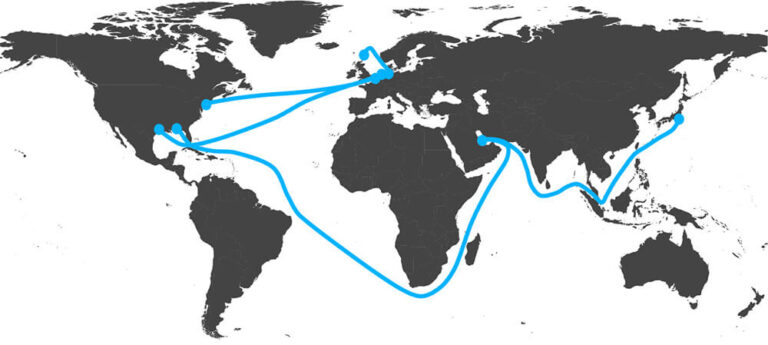

Whether oil, liquefied natural gas (LNG) or refined products, hydrocarbons travel by tankers that require about 30 to 60 (and for some routes, even 90) days to get from the Gulf to destinations that range across the globe; that is, to Europe, Africa, South Asia, East Asia and the U.S.

Notional – very cursory – chart of global tanker routes.

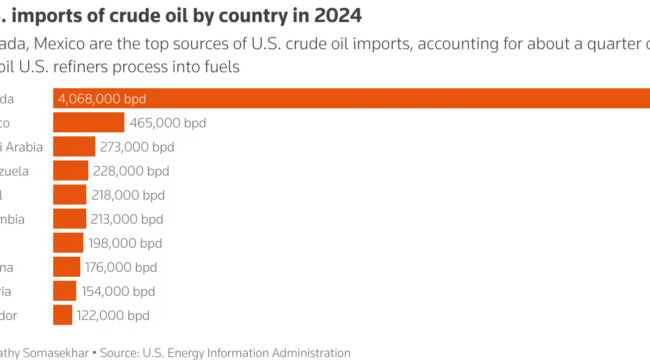

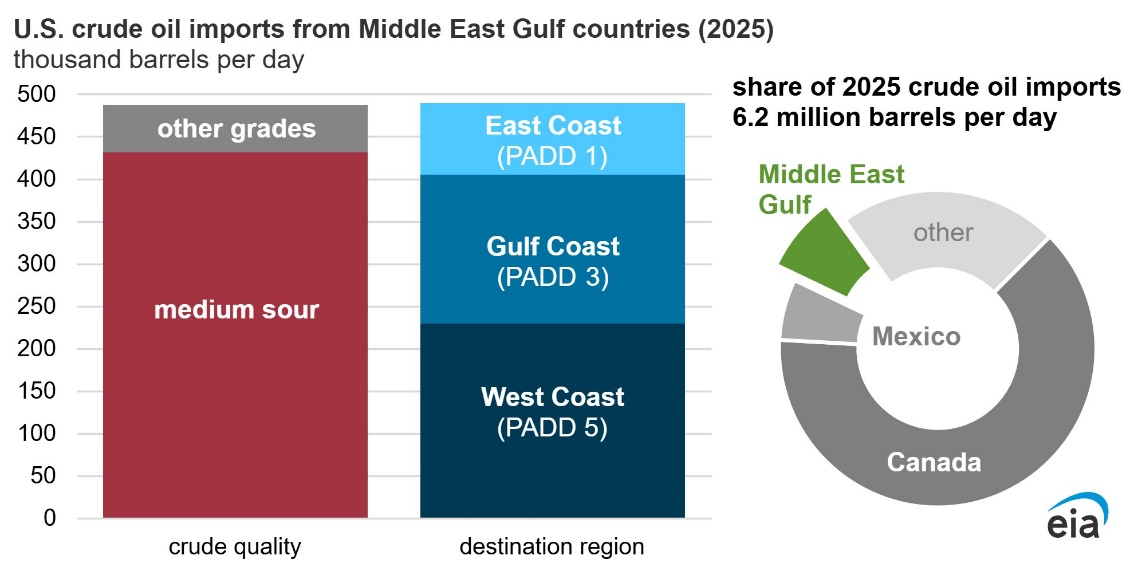

Along those last lines, and contrary to myth, the U.S. actually does (well, it “did”) import oil from the Middle East. In fact, last year about 8% of U.S. imports came from the Gulf region, just shy of half a million barrels per day. Here’s a breakdown:

U.S. oil imports, especially from Gulf nations., Courtesy Dept. of Energy/EIA.

Note that much of the imported oil from the Middle East is “medium sour,” which means it contains elevated sulfur, because many American refineries are geared to process that blend. And hold that thought as we get into other details about America’s imported oil barrels.

America’s Many Imported Barrels

First, as you look at that graph above of where America’s oil comes from, you can see that most imported U.S. oil – about four million barrels per day – comes come from a distant land known as Canada, namely the province of Alberta (see Alberta oil reserves in graph above).

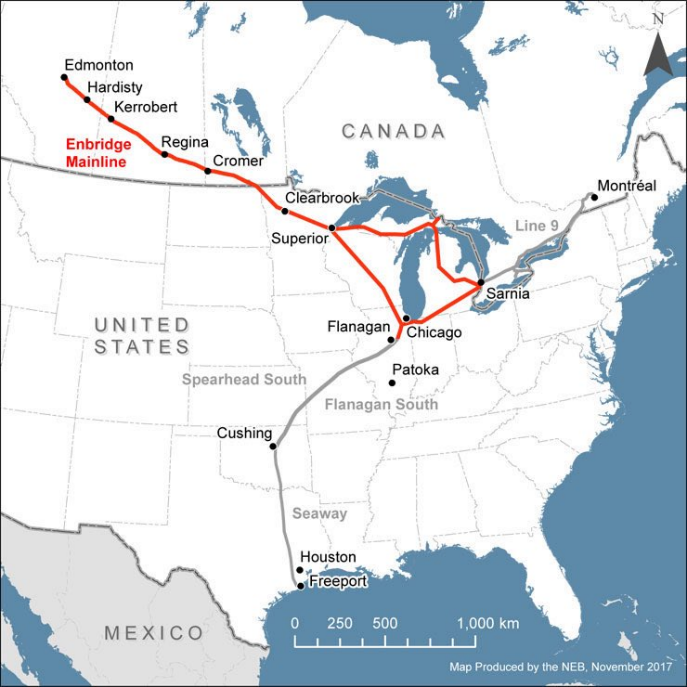

Now, here’s a map that shows one of America’s most important pipeline systems, namely the Enbridge Mainline out of Alberta, which moves about three million barrels per day of Canadian crude down into the U.S. Midwest. (And the overall system would be larger if President Biden had not – stupidly! – cancelled the Keystone XL line, back in 2021.)

Enbridge Mainline, moves Alberta crude oil to U.S. Courtesy @RazorOil.

Those three million Enbridge barrels per day are unmatched by any other pipeline in North America, even the Alaska Pipeline. In this sense, Canada is a critical part of making America “great,” if not an energy superpower: America’s Midwest and even Gulf coast refineries heavily rely on Canadian oil.

It’s worth pointing out that Alberta and its oil exports far outclass, say, Venezuela’s oil and that nations’ output of under one million barrels per day. If nothing else, Venezuela’s heavy, tarry, gunky oil must first be moved to the Caribbean coast and then loaded onto tankers for another sea voyage to Houston. So, on this point of logistics alone, Canadian oil is a blessing compared with other oil imports, even from relatively nearby venues like Venezuela.

Also, from that EIA graph above, note that not quite half of U.S. Middle East oil imports have been going to Gulf coast refineries, and not quite half to the West Coast, namely SoCal.

Those Gulf coast imports were mostly Saudi oil, headed to a Saudi-owned refinery near Houston. But the California oil imports? Again, much was Saudi but not all. And this highlights a serious problem in the U.S. West, namely the lack of local or even regional oil supply for California and its six remaining refineries (yes, only six left standing; it used to be over 40), as we see here:

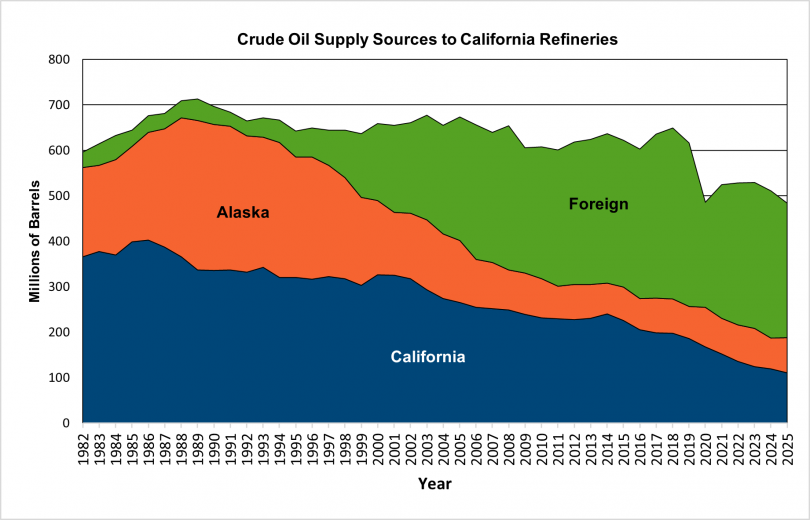

Oil supply to California refineries. Courtesy California Energy Commission.

Okay… What’s wrong with this picture? Well, until the early 2000s California produced most of its own oil, supplemented by output from Alaska. But not anymore. And that’s what’s wrong!

Over the past quarter century, California has taxed, litigated and regulated primary oil exploration and production down to bare bones, despite significant hydrocarbon potential in the state (long story). And the same goes for California refineries, many of which have closed over the past quarter century.

In other words, California has grown in population (well… until the past couple of years, as people left due to toxic politics). And as anyone who has recently been there can tell you – just ask me! – there are way more cars, trucks, trains, airplanes and everything else out there and burning fuel, despite the state’s so-called “green” efforts.

But as noted, California has way fewer refineries that are processing less and less oil supply from local or regional sources. And as you may know, California fuel prices are the highest in the nation; over $8 per gallon for diesel, I just saw in a news article.

The takeaway here is that much of the U.S. is (sort of) okay when it comes to physical supply of barrels. That is, most mid-continent and Gulf coast U.S. refineries have access to domestic, offshore and Canadian imported oil.

But out West is a very different story for California, and by extension for Nevada and Arizona, which obtain most of their refined products from California refineries or other imports.

West Coast Will Soon Have BIG Problems

So far, we’ve covered a lot of ground in terms of oil and where it comes from, and how it gets refined.

One big takeaway is that California has an oil and refinery problem. Most oil that flows through California refineries is imported. And now, global events have disrupted that trade. But also, and because California has so few refineries, the state also imports significant amounts of refined products. From where? Oh, man…

Until recently, much of California’s diesel fuel was imported from South Korea (yes, seriously). That is, oil would go from, say, Saudi to Korea, get refined, and then move across the Pacific Ocean to California. But considering the Iran war, that’s all coming to a halt.

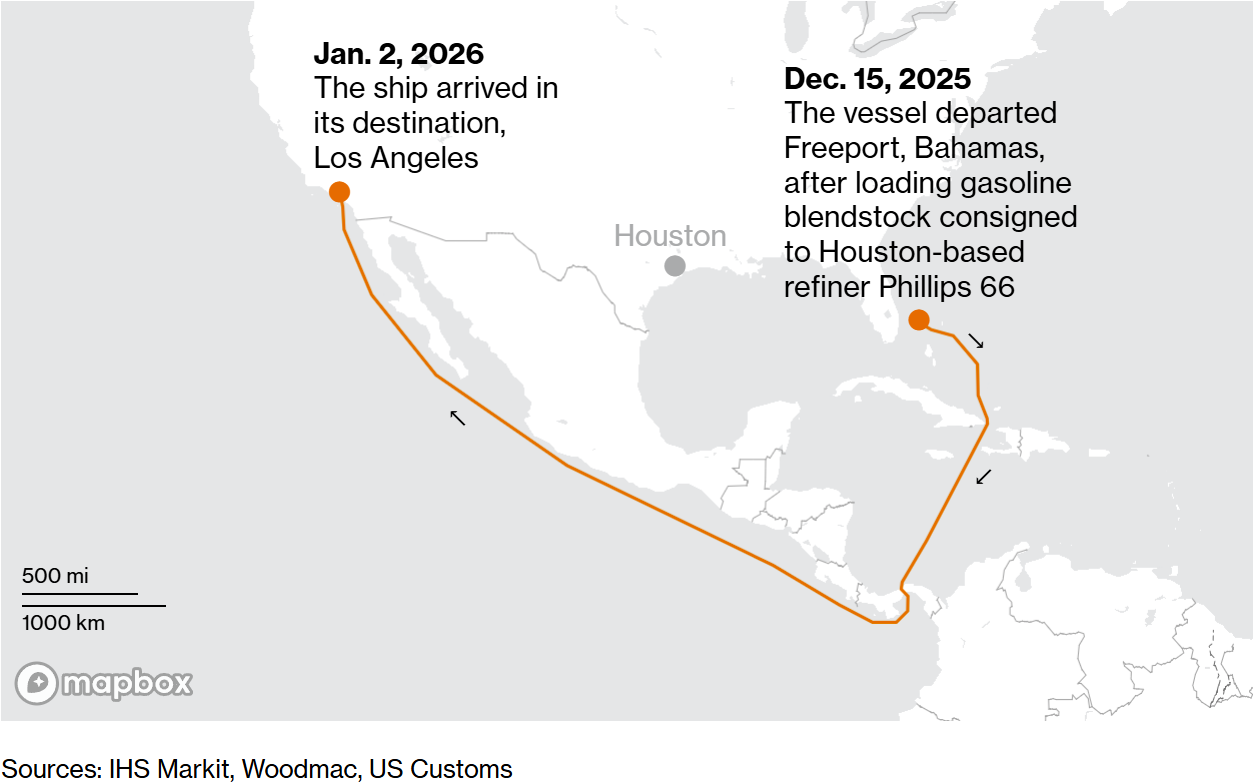

Another source of refined products for California is the U.S. Gulf coast, although it’s a circuitous route via Bahamas (due to the Jones Act – long story) and then a transit through the Panama Canal.

Recent refined product shipment from Houston to Bahamas to California. Courtesy Bloomberg News.

Look at it this way: California is a geographically isolated market. What makes it worse is that much of the refined products in Arizona and Nevada also originate from California. So, looking ahead, the West coast and adjacent states can expect much higher prices for gasoline and diesel fuel.

Of course, right now everybody pays more for fuel; I mentioned earlier that we had a 30-cent per gallon increase for diesel just last week, here in Pennsylvania. Clearly, diesel fuel prices are rising nationwide, but those fuel prices are way higher in California, and it’s all about to get worse.

Go back to those above-mentioned 90-day tanker runs for crude oil from the Middle East. Well, all those oil tankers that didn’t sail in early March, because of the war and blockage of Persian Gulf, are now NOT arriving at unloading piers across the world, from Pakistan to New Zealand to… yes… not to the unloading piers of California.

And without crude oil, refineries across the world lack feedstock to run through the cracking towers. Thus, in 15, 30, 45 days or so – end of April, early May – refined products will run short across many parts of the world, and likely in the U.S. West.

Already, Asia is slowing down:

- The Philippines has declared a national emergency, with fuel reserves under 5 days.

- Pakistan has declared a four-day work week; situation is desperate.

- Bangladesh has imposed curfews to stop fuel-burning activities past 6:00 pm.

- Thailand has shut down much of its fishing fleet for lack of diesel fuel.

- Even China has lines at filling stations, and has banned fuel exports, including to Australia and New Zealand which are at the far end of every sort of oil and refined product supply chain.

Is this doom and gloom? Yes; sorry. But the fact is that energy will drive inflation, or as noted above, “dieselflation.”

And there’s a lesson here for nations everywhere: don’t have dumb, kneejerk, bumper sticker energy policy; drill your own freaking oil, build your own freaking refineries, and always be nice to Alberta.

Meanwhile, looking ahead, “What’s the real price of oil going to be?” people ask…

Well, there are paper barrels that trade on the exchanges. And then there’s real crude, like what’s currently not moving in large volumes out of the Persian Gulf. Which means that across the globe – see that nice photo topside – oil refineries that want crude must pay up for petroleum.

Brent-contract barrels (one key international standard) are going for as much as $160, per data I saw the other day. And I’ve heard tales of tankers on Asian routes making three and four course changes to different destinations, as refineries bid for barrels. It’s wild out there.

Meanwhile, if you are in the U.S., be glad! At least we have barrels and fuel here. Compare with Australia, with just two refineries and not nearly enough domestic oil to keep the planes, trains and autos running. And definitely be glad you’re not in New Zealand, with zero refineries, and which must import every drop of refined fuel and lubricant.

And for investing? Keep it simple: oil companies with minimal exposure to the Middle East, like Petrobras (PBR), and U.S. domestics. Plus, oil services like Schlumberger/SLB (SLB), Halliburton (HAL), or the OIH fund. (Of course, these are not official reccos; we don’t have a Reckoning portfolio.)

That’s all for now. Thank you for subscribing and reading.

Comments: