Money to be Made in ‘Boring’ Metals

The last year has been a precious metals story.

We’ve covered that story to the point that even I’m getting sick of writing about it.

Thankfully, things are heating up in industrial metals. And there are some attractive opportunities in cheap mining stocks.

With the industrial metals we’re talking about iron, aluminum, nickel, copper, zinc, etc. Hard assets.

These are the “boring” metals, but right now they look pretty darn exciting. Check out the 1 year chart of nickel:

Source: Trading Economics

Well, that’s not a very boring chart, is it?

Nickel is a key industrial metal, and it’s currently trading around $18,000 per ton. Nickel’s primary use is in stainless steel, but it’s also important for rechargeable batteries, aerospace, and many other applications.

The largest nickel miner in the world is Russia’s Norilsk Nickel. But since it’s a Russian company, that one is currently uninvestable.

Vale: One Way to Play the Industrial Metals Boom

The second largest nickel miner is a name you might recognize: Vale (NYSE: VALE). Vale is the Brazilian mining giant we covered in depth back in June of last year (disclosure – I own it).

Since that article, Vale is up about 38%. But shares are still down more than 60% from their 2008 high, and the dividend yield is substantial at around 5% (with room to grow if commodity prices keep rising). The company currently trades at just 10x earnings, and 7x 2026 estimates so it’s still in what I consider the “very cheap” zone.

Vale produces a lot of nickel, but it’s mostly an iron ore miner (a much larger market). Here’s a chart of iron ore prices over the last 10 years.

Source: Trading Economics

This chart does not account for inflation. Once you factor in all the inflation that’s happened over the last decade, iron ore is cheap today. And Vale has some of the lowest costs and highest grades.

Vale is also the world’s 2nd largest in nickel, and there’s a material amount of copper, cobalt, platinum, and gold and silver too. And the company owns a massive transportation and distribution network. Ships, railroads, ports, etc.

On the risk side, Vale does have a lot of debt. And I’d like to see them reduce that over time. But the company is highly profitable and can service it. One other risk worth noting is the Fundao dam collapse, an environmental disaster at a site owned 50/50 by Vale and BHP. A 2024 court ruled that the companies would have to pay $30 billion over 20 years for cleanup and to compensate people in affected areas.

However, at current levels I believe all the risks are already priced in. I plan to hold this stock, and reinvest the dividends, for many years to come.

Vale is a relatively high-risk, high-reward vehicle to bet on industrial metals (mostly iron with a side of nickel and copper).

We’ll explore more ways to invest in industrial metals soon.

What Drives Base Metals?

The primary factors which will determine the direction of industrial metals are:

- Monetary Policy

- Sanctions and trade wars

- China’s economy

The first one is simple. If the Fed keeps cutting rates and QE continues or accelerates, the dollar should fall. This is basically money printing, and bullish for commodities. Quite likely, in my view.

The second one is more complex. The world is moving into a trade war posture. Export controls are going into place worldwide, after a long period of relatively free trade.

Trade wars are a complete wild card. China just put export controls on silver, which nobody would have expected a year ago.

Anything could happen in this geopolitical environment. The world is in flux.

The third factor is also tricky. It’s the fate of the world’s, and especially China’s, economy. For now at least, China is the world’s factory, and a fast-growing consumer economy themselves.

China accounts for about 50% of all global industrial metal demand.

Chinese exports are a big part of it, but their domestic growth has been massive over the past 30 years.

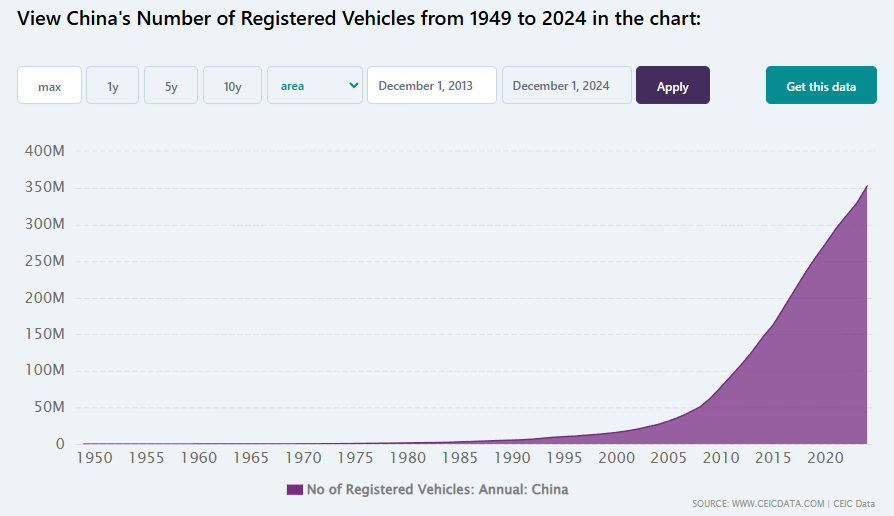

For example, take a look at the chart below, which shows the number of cars registered in China.

Source: CEIC

As you can see, China went from basically no cars in 1995 to more than 350 million today. That is a LOT of additional demand for base metals.

So despite China’s recent woes and property bubble, their economy has grown incredibly fast over the longer term.

China is an important part of the industrial metals bull case.

Less Poor

Industrial metals are essentially a bet on people in the world getting less poor. Not rich, just not in poverty.

A house or apartment, bikes, maybe even a car. It all adds up with billions of people.

This story of less poverty, and larger middle classes, is playing out across the world. But it has been particularly acute in China.

Patience May Be Required

If we get a major stock market crash and recession, that would temporarily dampen demand for industrial metals. But soon, governments and central banks would be printing money to stimulate lagging economies, supplying stimulus, and building infrastructure.

That would weaken fiat currencies, driving up metals prices. And it would stimulate demand for building supplies, autos, etc.

In the short term, the direction of industrial metals is hard to predict. But I’m convinced that we will see substantial inflation within the next few years, and hard assets should be a great place to hide out.

Industrial metal miners are out of favor, cheap, and starting to show life. In my experience, that’s a very good combination. But sometimes this method does take patience.

Eventually base metals will rise, and quality companies that produce them will too. It’s just a question of when. We might be early on this one, which would be fine. I will hold and let the dividends compound at cheap prices.

Eventually base metal miners will be re-rated higher.

I’m spending quite a bit of time lately researching base metal miners, so look for more updates soon.

Comments: